Our latest study of shifts in compensation plans before and after technology and life sciences firms go public reveals interesting trends in equity compensation strategies.

Starting in 2010, Radford's compensation consulting team began tracking US-listed initial public offerings (IPOs) in the technology and life sciences sectors to examine key shifts in compensation strategy occurring just before and after IPO events. Such shifts include the adoption of new, more flexible equity incentive plans, changes to pre- and post-IPO equity overhang rates, the creation of broad-based employee stock purchase plans (ESPPs), and adjustments to executive officer compensation.

Today, Radford's database of recently public companies includes information for a total of 410 organizations that went public between January 1, 2010, and December 31, 2014. During this five-year period, technology and life sciences companies raised a median of $75 million by virtue of selling shares to the public, while having a median pre-IPO headcount of 246 employees and median pre-IPO annual revenues of $46 million.

The following research excerpt from Radford's five-year study, produced with data collected from public Securities and Exchange Commission (SEC) filings, explores pre- and post-IPO equity overhang rates and their importance for judging the overall health of equity compensation programs at recently public companies.

Overhang under the Microscope

In today's environment of increased investor scrutiny, managing equity overhang rates while on the road to becoming a public company is vital. While private firms tend to have more flexibility to establish and fund equity compensation plans with the blessing of a small group of investors, public companies must obtain the approval of a much broader base of shareholders with diverse standards for equity compensation programs.

As result, when handling the transition from private to public environments, companies are typically under intense pressure to quickly moderate their use of equity compensation. Monitoring "equity overhang rates" at recently public companies can provide critical insights into what is an acceptable rate of equity usage as an organization matures and prepares to go public.

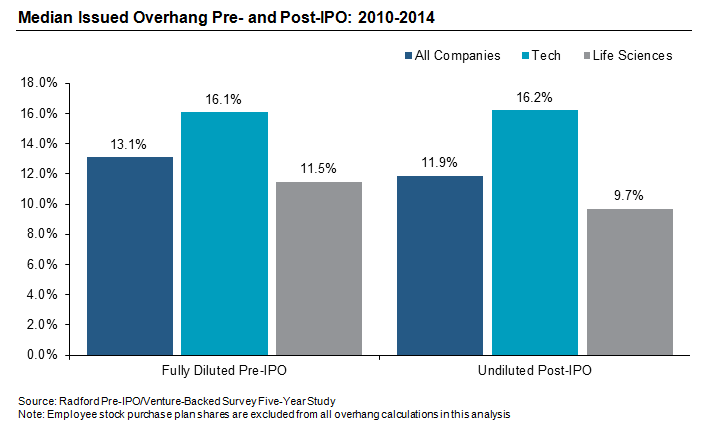

Overhang rates can be measured in several ways. One measure commonly used by Radford is "issued overhang." It shows the potential dilutive effect of outstanding employee stock options and restricted shares on existing shareholders. Outstanding employee awards are those that have been granted to employees, but have not yet been settled (e.g., unexercised options or unvested restricted stock).

At private, venture-backed organizations it is common to express equity overhang rates as a percentage of "fully-diluted" common shares outstanding, which includes the employee equity awards in the denominator of the calculation even though they are not yet settled (i.e., the outstanding employee awards are in the numerator and the denominator). The convention for public companies is to use an "undiluted" measure, with only common shares outstanding in the denominator.

As the chart below illustrates, issued overhang rates typically drop after an IPO. This occurs because the total number of shares outstanding at the company rises once shares are sold through the offering. The drop-off effect is most noticeable at life sciences companies, where a greater percentage of the company is typically offered in the IPO. In a sector vs. sector comparison, issued overhang rates are higher at technology companies, where equity compensation is often used more broadly and aggressively.

The issued overhang measures described above are calculated as follows:

- Fully-Diluted Pre-IPO Issued Overhang is calculated as:

- Undiluted Post-IPO Issued Overhang is calculated as:

Total Overhang

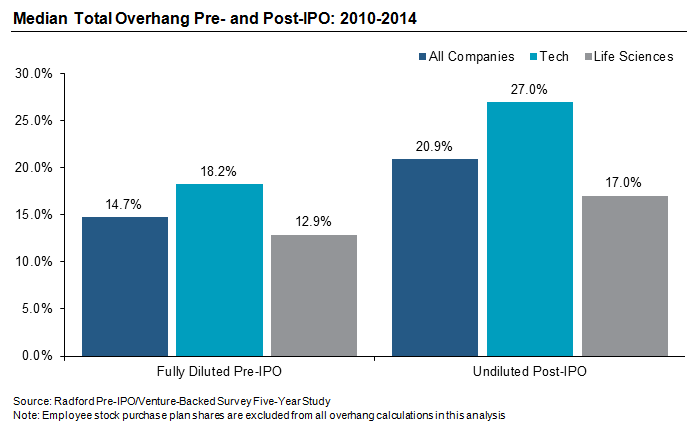

"Total overhang" is another overhang measure frequently used by Radford. Total overhang provides a more comprehensive view of potential shareholder dilution by taking into account the entirety of employee equity programs. This is calculated by looking at shares available for future grants, along with outstanding employee stock options and restricted shares. The same issues with respect to "fully-diluted" and "undiluted" measures remain when considering total overhang rates at pre- and post-IPO companies.

Unlike issued overhang, total overhang rates typically increase at the time of an IPO. This occurs because companies often introduce new equity compensation plans with fresh funding at the time of an IPO. Again, like issued overhang, total overhang rates at technology sector companies tend to be higher when compared to life sciences companies because of larger employee equity participation rates and levels.

The total overhang measures described above are calculated as follows:

- Fully-Diluted Pre-IPO Total Overhang is calculated as:

- Undiluted Post-IPO Total Overhang is calculated as:

With the latest year of data added to our study, we find total overhang is larger for both technology and life sciences companies after they go public, however, there is little change in issued overhang between the pre- and post-IPO time period. The newest update to our research provides valuable data on equity compensation trends for companies as they consider an initial public offering.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.