The addition of new metrics is a welcome sign for companies eager to see ISS move past its sole reliance on TSR, but in some industries, like pre-commercial biopharma, the new metrics won't make a lot of sense.

Institutional Shareholder Services (ISS) has announced that it will include six new financial metrics in its pay-for-performance assessment for Say-on-Pay voting recommendations. Initially, the new metrics will be part of the qualitative screening process, but we won't be surprised if they are introduced into ISS' quantitative screening methodology in the future.

Institutional Shareholder Services (ISS) has announced that it will include six new financial metrics in its pay-for-performance assessment for Say-on-Pay voting recommendations. Initially, the new metrics will be part of the qualitative screening process, but we won't be surprised if they are introduced into ISS' quantitative screening methodology in the future.

The additional metrics will apply for companies in the US and Canada beginning on February 1, 2017. Proxy reports will now include a standardized table containing a company's three-year performance relative to its ISS-selected peer group on: invested capital (ROIC), return on equity (ROE), return on assets (ROA), revenue growth, EBITDA growth, and growth in cash flow from operations.

The weighting of each metric will vary by industry, but those weightings are not yet publicly available. The firm will calculate relative three-year performance for each metric against peers, and as compared to relative compensation levels. ISS will then provide a standardized comparison of financial performance ranking and CEO pay relative to the peer group in the form of a numeric result. This number is intended to demonstrate the alignment between three-year performance and three-year granted pay.

For certain companies, like those in the pre-commercial biopharma industry, many of these new revenue-driven metrics aren't relevant, as these companies are not yet generating meaningful revenue and there are other, more meaningful benchmarks of company success. ISS has indicated that it won't apply all six metrics to industries where they don't make sense, but has not provided specific details on this issue. While compensation professionals should begin to review how performance is measured using these new metrics, and how it aligns with compensation on an absolute and relative basis, companies should consider whether or not these metrics are appropriate indicators of success in their industry. We encourage our clients with concerns about how these new metrics will be used to evaluate their pay-for-performance alignment to reach out to ISS and express their views, particularly in instances where these metrics will not provide a meaningful representation of performance.

On the flip side, there are many technology and life sciences companies that likely will benefit from the introduction of additional performance metrics into ISS' pay-for-performance analysis. Many companies and institutional investors have expressed concern about the homogenization of performance-based equity plans that are linked solely to stock price performance. There is no question that this shift was driven in large part by ISS' focus on relative TSR when assessing the alignment between pay and performance. ISS' decision to take a broader perspective with respect to assessing performance should provide companies with additional confidence in selecting alternative metrics to better align incentive payouts with company performance.

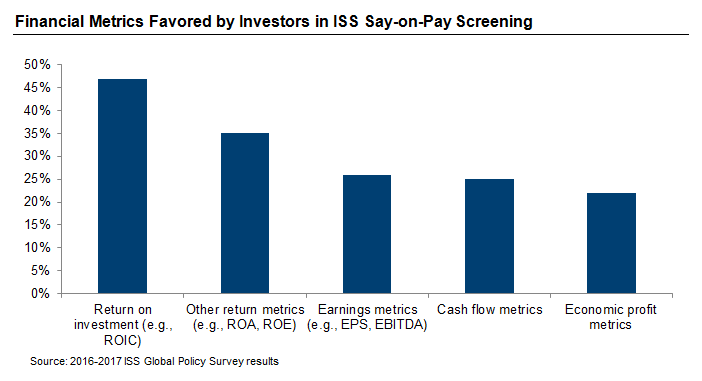

During its policy survey process this summer, ISS asked companies and investors about using other performance metrics in addition to TSR. Nearly 80% of investors and 70% of companies supported the use of other metrics. The following chart, from the ISS survey, shows investor support for using specific financial metrics:

If a company's Compensation Discussion and Analysis (CD&A) disclosure has not previously discussed the company's performance for the year as measured by the new ISS metrics, we recommend considering the inclusion of this information. Doing so will provide companies with an opportunity to demonstrate how aligned operating performance and stock price performance are, provide context to assist shareholders in their assessment of performance, and more clearly link compensation with performance in the eyes of shareholders.

Window to Update 2016 Peer Group Open

In separate ISS news, the proxy advisory firm has opened up the submission period for companies to share updated peer groups if they’ve made any changes this year. The window is open from Nov. 28 to Dec. 9.

ISS’ pay-for-performance assessments involve comparisons to an ISS-constructed peer group. US companies have a chance to submit their own self-selected peer groups used in setting 2016 compensation in order to inform ISS of their self-selected peers. Since ISS began taking these submissions, the overlap between companies’ own peer groups and ISS’ peer group has increased significantly— a development we view as positive.

Canadian and European companies that are now subject to a pay-for-performance assessment may also submit self-determined 2016 peers for the first time.

Next Steps

We will continue to monitor and update our clients on the impact of the addition of new financial metrics to ISS’ qualitative screening process, including the influence on Say-on-Pay recommendations and voting outcomes. In the meantime, to speak with a member of our compensation consulting group about these changes or other executive compensation issues, please write to consulting@radford.com.

Related Articles