Assessing your sales compensation plan mid-year provides time for business and sales leaders to agree on a set of principles upon which to design the program.

It's tough to start working on something with a distant deadline. It's like focusing on your taxes in November. But chances are that others in your organization also think that the annual plan redesign process has to start before October to be effective. I recommend beginning the midyear planning process by making sure business leaders have agreed upon a set of principles and standards for an effective program. It can be a long process to secure leadership consensus on matters that, in some cases, are philosophical. If leadership has clearly stated its intent for the program and agreed to the measures for comparing the program's output with the intent, then you have a key lever for getting started.

Data Drive the Process

If your company uses a calendar-year cycle for managing its plans, sales leadership probably does not start thinking about plan changes before the fall, unless there is some perceived dysfunction that requires attention sooner. However by midyear, your systems have ideally collected enough data for an objective perspective on the program's health. In general, we're talking about employee pay and performance data.

At Radford, we use three primary measures to assess plan effectiveness:

- Compensation cost of sales (CCOS). Think of this measure as your program's check-engine light. A CCOS score outside of your predetermined limits— to use the analogy akin to a red light— won't tell you what specifically is wrong, only that the program needs attention. CCOS is the amount spent on sales compensation as a percentage of the program's revenue. The cost component, or numerator, includes all employees on the program (e.g., managers and overlay roles). The revenue component, or denominator, includes pure production with no double counting.

If the percent score is increasing, this means cost is rising at a faster rate than revenue (or revenue is decreasing faster than cost). There are myriad reasons why this can happen. But like the innocuous little red engine light on your car's dashboard that that can glow for months without incident, a high or low CCOS score requires some analysis and explanation.

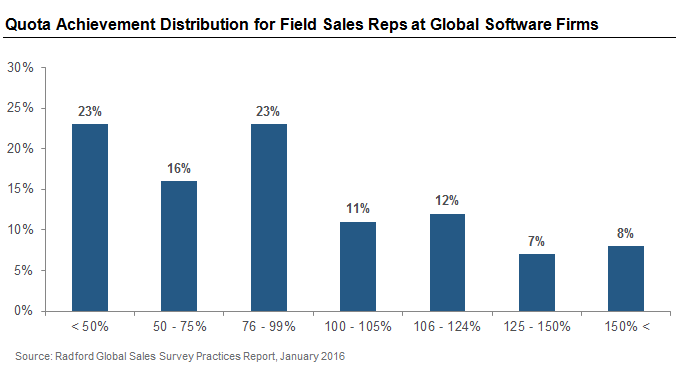

- Employee performance distribution. This measurement is more specific than CCOS and gets at your program's motivational impact and, if the plan is quota based, cost effectiveness. A good distribution, as read through a histogram, is one that aligns with your company's philosophy and defines the appropriate curve. It provides a meaningful differentiation of performance without establishing unique classes of A bad distribution is one that's not centered on or near 100% attainment; in other words, a standard that's reasonable for midyear but not year-end (e.g., 50%). This would suggest that quota attainment is a poor measure of performance. A left- or right-biased distribution says quotas are too high or too low – meaning the company is paying too little or too much for its talent. Finally, a bimodal curve, with a concentration of people performing below and another group concentrated above quota, suggests you may have 2 different jobs roles that are being treated as 1. There is no quick fix here, only recognition that quotas may not be effective in motivating people or managing costs. A good place to start is on the quota allocation and adjustment policy.

The chart below illustrates a sample quota achievement distribution of software technology companies using the Radford Global Sales Survey. The data indicate a large number of sales representatives are failing to meet their target goals.

- Employee pay and performance correlation. If the bulk of your company's program uses plans that dedicate 50% or more of the target incentive to a single measure, such as sales quota attainment, then a scatter plot (each plot represents an employee) of total incentive pay versus quota attainment provides a quick indication of alignment between the two. If your plans use a variety of performance measures and not one is prominent, then you have multiple ways of defining success and can't use this type of analysis for your program. Ideally, there is a strong correlation between quota attainment and pay (as a percentage of target pay). When the correlation falls, it's often because of an increase in pay from non-quota sources such as Sales Promotion Incentive Funds (SPIFs).

Standards Put Data into Action

Those three key measurements of sales plan effectiveness, in addition to other measures that may be specific to your business, require standards to help define whether a measure's score is good or bad. Otherwise, the data are interesting but not actionable. Companies often credit a meaningful sales compensation philosophy that is supported by program objectives as a critical factor for a strong design process. This philosophy should be a statement of intent supported by measures that help determine how well the plan is working— that is, standards for performance.

For example, leadership states through its design philosophy that quotas will be challenging but motivating. The measure of performance for motivating quotas is quota attainment distribution. Specifically, more than 50% of salespeople falling short of quota in two consecutive years indicates the program is not meeting the standard. A standard deviation less than 20% of attainment suggests quotas may not be sufficiently challenging, while above 50% of quota attainment suggests quotas are unreliable for measuring individual performance.

Many standards for program performance are supported with competitive benchmarks. Target pay is the most common benchmark. The Radford Global Sales Survey goes beyond pay and report averages for employee quota distribution and CCOS.

When defining and using standards for program performance, less is often more. A guideline is to use five brief statements to define how leadership views an effective program, with multiple objective standards for measuring program performance. Keep in mind, leadership must agree to the philosophy— and sales management will need to convincingly articulate that philosophy— for it to have impact.

Next Steps

For companies in a calendar year sales compensation cycle, midyear is a great time to assess your compensation plan relative to expected outcomes. While doing so requires more work on the front end of the sales compensation review process, it will save you time in the fall when sales leaders begin reviewing potential changes to the plan for the following year.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles