The SEC Corporation Finance Staff, on September 21, 2017, issued three forms of guidance on the CEO Pay Ratio Rule: an interpretive release, a press release, and new and revised C&DIs.

This long-awaited guidance was released just nine days prior to October 1, 2017, which is the first date that calendar year filers may select as their median employee determination—that is, nine days before many calendar year filers intend to calculate their median employee, and weeks or months after many issuers have begun to prepare for this new disclosure.

While much of the new guidance simply restates prior guidance (whether given through the adopting release or prior C&DIs from October of last year), several points stand out:

- Identifying Employees and Independent Contractors: The guidance clarifies that companies may determine who is an employee under the rules by applying a widely recognized test under another area of law. Presumably, if an employer has correctly determined that an individual’s compensation should be reported on Form 1099 rather than Form W-2, then we would expect that individual to not be included as an employee. Effectively, companies can now determine who is an employee for purposes of the rule based on whether they receive a W-2.

- Reasonable Estimates: Staff clarified that the pay ratio may be presented as an estimate. While this does not impact the actual process of identifying the median employee, it is an apparent nod to imprecision built into the median identification. This includes the use of reasonable estimates for calculating elements of the median employee’s compensation. The end result of this pronouncement is that companies may rely on reasonable estimates, though the use of such estimates must be disclosed and verified.

- Statistical Sampling: The new guidance provides clarifications concerning sampling, details of other reasonable methods, and some examples of both. This is likely most applicable and helpful for companies with overseas workforces or those with non-centralized payroll systems.

Observations in the Banking Industry

Many banks are in the midst of identifying their employees and performing preliminary calculations. As they pursue various methodologies to determine their CEO Pay Ratio, we have observed several emerging trends:

- Independent Contractors: Prior SEC guidance suggested that the definition of an employee be focused on whether or not the company determined a particular worker’s compensation. Without a centralized means of identifying independent contractors or a reliable method to identify how pay was set in each case, many banks struggled with this issue. The most recent guidance provided clarity on this issue and has significantly streamlined the employee identification process for many banks.

- HRIS Systems: The relative usability and sophistication of a bank’s payroll or human resources information systems has been a key determinant in the pay ratio process. Banks with centralized systems containing necessary data to conduct the process are waiting longer in the October 1st to December 31st timeframe to identify employees and determine their median employee.

- Dry Runs: Banks have been doing “dry runs” or pro-forma pay ratio calculations to work through the process, while providing the management and compensation committee with estimated pay ratio results. The focus is on identifying and documenting a workable methodology that appropriately balances administrative and technical concerns. A future change in methodology would require disclosure to shareholders, which banks wish to avoid. Depending upon systems, pro-forma calculations are based upon either 2016 data or, if systems can support it, a more sophisticated approach based on estimated 2017 data.

- Annualizing: There are a number of rules relative to how pay can and cannot be annualized. This is interrelated to how and when a bank determines its median employee, e.g., whether full-year or partial-year data is used, and what date in the October 1st to December 31st timeframe is chosen to identify employees. For example, banks using year-to-date pay have struggled to reconcile a dataset that incorporates employees who receive an incentive payout once per year and others who receive payouts on a quarterly or monthly basis. Decisions on how to handle annualizing must consider the SEC rules, which do not allow full-time equivalent adjustments for part-time employees or annualizing for seasonal or temporary employees.

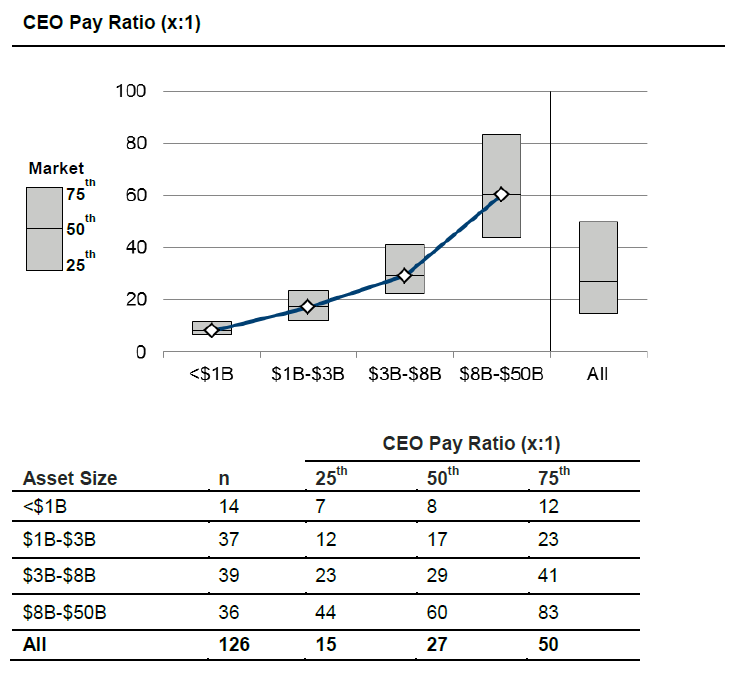

- CEO Pay Ratios for Banks: For banks below $50 billion in assets, the median pay ratio is expected to be less than 60:1, as shown in the chart below. The actual median employee compensation depends on the business model of the bank. Those that are more retail focused with larger branch networks, typically have a lower median employee, often between $40,000 and $50,000. In contrast, commercial focused banks with smaller branch networks are likely to have median employee compensation in the $50,000 range. The actual median employee level will vary dramatically based upon geographic location and business model, with the ultimate ratio more highly contingent on CEO pay levels.

Details on the New SEC Guidance

Identifying Employees and Independent Contractors

The staff withdrew its prior guidance in the form of C&DI 128C.05, which clarified that contractors whose compensation was determined by an unaffiliated third party are not employees for purposes of the ratio. In its place, the interpretive release indicated that the ‘unaffiliated third party’ test is not intended to exclusively determine whether a contractor is an employee, adding that “to apply a widely recognized test under another area of law,” citing, as a non-exclusive source, wide-ranging IRS Publication 15-A Employer’s Supplemental Tax Guidance (2017) on this issue. Importantly, Publication 15-A in its definition of independent contractors, adopts a test based on control rather than power to set the contractor’s rate (as was used in the withdrawn C&DI). This may significantly impact prior determinations of who must be included in the employee population for purposes of the CEO pay ratio. Presumably, if an employer has correctly determined that an individual’s compensation should be reported on Form 1099 rather than Form W-2, then we would expect that individual to not be included as an employee. The same type of decision making may also apply in non-U.S. situations.

Reasonable Estimates

In C&DI Q 128C.06, the staff clarified that the pay ratio may be presented as an estimate. This guidance allows companies to confirm their disclosure to the reality of the new disclosure requirement, and therefore may rely on reasonable estimates provided there is a basis for doing so and the use of estimates is disclosed. Additionally, the interpretative release states that “if a registrant uses reasonable estimates, assumptions or methodologies, the pay ratio and related disclosure that results from such use would not provide the basis for Commission enforcement action unless the disclosure was made or reaffirmed without a reasonable basis or was provided other than in good faith.” Companies considering whether to include estimates should determine if their use is necessary, and how such estimates will be viewed by investors and other outside audiences.

Statistical Sampling

Under earlier guidance, the SEC permitted companies to engage in sampling and / or other reasonable methodologies, though guidance was vague. The new guidance provides clarifications concerning sampling, details of other reasonable methods, and some examples of both.

Our Advice

The following points may be noteworthy for many issuers:

First, the SEC reaffirmed that, should a company choose to engage in sampling and / or other reasonable methods for completing their CEO Pay Ratio, the sampling must be based on the registrant company’s facts and circumstances, rather than broad or industry averages. However, all of a registrant company’s exact compensation information does not need to be available to perform the CEO Pay Ratio analysis. The guidance states that in cases where registrants do not wish to rely on the exact compensation data for a given business unit, a distribution assumption could be employed instead. That is, registrant companies would make an informed assumption about the distribution of their specific underlying compensation data. The SEC indicated that many common distributions might be appropriate, including combinations of distributions. The requisite parameters needed to develop the distribution would be inputted from a reasonable, company-specific approach. In an example from the guidance, input from regional managers would aid in developing those parameters. The company would then use this distribution in place of the actual data.

We believe that this distribution assumption example might be particularly useful for registrant companies with multiple global HRIS systems, with or without employing an overall sampling approach to determining the CEO Pay Ratio. In fact, the updated guidance explicitly approved using reasonable methods for some units and alternate methods for other units, provided the approach is reasonable. A company should not feel wedded to one approach for the entire employee population. In cases where it might take three to four weeks to acquire data for a business unit, or where companies rely on division managers as part of the data obtaining process, we recommend developing a distribution assumption for that business unit’s data as a simplifying assumption to ease administrative burden.

Related Articles