To date, no company has won or lost vote support as a result of their pay ratio disclosures. With proxy advisory firms remaining silent on this issue so far, we don’t expect that to change.

Most companies listed in the United States are disclosing their CEO pay ratio for the third year and, so far, the disclosure has largely been a sleeper issue. Nevertheless, in this article we share insights on disclosure issues that companies must consider in order to remain in compliance with the letter and spirit of the rule; observations concerning median employee compensation (the only new piece of information produced by the rule); and examine an emerging activist campaign that, despite its relative lack of impact to-date, could potentially change the direction of pay ratio disclosures in the future.

Disclosure Issues Companies Must Consider

In the first year of pay ratio, the principle question on companies’ minds was: “Who is the median employee?” As the pay ratio disclosure is a simple ratio of CEO pay and median pay, and CEO pay was already known and reported, the bulk of the effort of producing the CEO pay ratio rests on the identification of the median employee. This question is not as simple as it sounds, as the rule provides for a handful of estimates and exceptions that can influence the identification of the employee who will serve as the median. The principle questions involved in identifying the median employee are:

- What is the appropriate estimate of employees’ compensation (“Consistently Applied Compensation Measure” or “CACM”)? This measure must be reasonably representative of the compensation of employees of the company. For example, we find that in sectors that grant equity broadly, equity should generally be included in the CACM. In other sectors with a larger population of non-equity eligible employees — such as retail — wages, or a reasonable estimate thereof, may be more appropriate.

- Which employees are included in determining the employee population from which the median employee is selected? The rule generally provides that all worldwide employees, except the CEO, must be included in the employee population, unless certain exemptions are applied. First, the company may apply any widely recognized legal definition in determining what it will define as an “employee,” which could influence the outcome. Most appear to employ the IRS’s relatively narrow definition. However, some classes of foreign employees may, and frequently do, require additional inquiry. Additionally, firms may choose to exclude up to 5% of their foreign-based employees, under limited circumstances (the “de minimis” exemption), and may exclude certain other foreign-based employees under even more limited circumstances (the “foreign privacy” exemption). Moreover, employees of a firm acquired during the year in review may also be excluded at the election of the company (the “merger” exemption). Each of these decisions strongly influences how the company approaches its pay ratio disclosure obligations in the following year. Moreover, if more than one of these exemptions are applied, there may be overlap that must be accounted for.

- What if the median employee, identified above, has aberrant compensation? Frequently, the identified median employee’s actual compensation will be significantly above or below the CACM estimate, or relative to that of the immediately surrounding employees. In 2017, prior to the first pay ratio disclosure, the SEC expressly opined on this point, allowing discretion to substitute a different employee. However, there are no objective standards to inform the inquirer as to whether the identified median employee’s compensation is “aberrant,” and what an appropriate substitute would be.

The CEO pay ratio rule permits the use of a median employee for up to three years, under certain circumstances. The first set of circumstances has to do with whether the company used exemptions in the prior year that require it to identify a new median employee. If either of the following apply, the company must re-identify its median employee:

- Did the company apply the merger exemption in the prior year? If the company excluded employees in the prior year that became employees as a result of the application of the merger exemption, it must re-identify its median employee, with the excluded employees included in the employee population. It does not matter whether five or 5,000 employees were previously excluded under this exemption — the median must be re-identified in any event.

- Was the de minimis exemption applied in the prior year? Prior use of the de minimis exemption does not itself result in the requirement that the company re-identify its median employee, but the analysis does not stop there. The de minimis exemption provides that the company may exclude up to 5% of its employee population, all of whom must be foreign-based, provided that those employees are excluded on a whole-country basis (meaning if one German employee is excluded, all German employees must be excluded). However, if the number of excluded employees significantly increased vis-à-vis the prior year’s population, the exemption may become unavailable to the company. This is a fact-specific analysis.

Provided the company determines it is not required to re-identify its median employee because of its prior use of one of the exemptions above, it must then determine whether its prior identification remains relevant. Companies are permitted to re-use their previously identified median employee if they can affirmatively determine (and disclose) there has not been a significant change to its employee population, or a significant change in its employee compensation arrangements, that the company believes would result in a significant modification to the pay ratio disclosure. The following two questions must both be answered in the negative:

- Has there been a significant change in the employee population that would significantly impact the identification of the median employee? The SEC has not provided guidance to assist companies in determining what would constitute a “significant change” that would “significantly impact” the identification of the median employee. However, experience indicates that simply reviewing the net increase or decrease in the employee population (even if assumed to be “significant”), does not necessarily mean that the change in population will significantly impact the median employee. For example, if a company’s headcount increased or decreased by net 10%, but that increase or decrease was evenly distributed around the median, then there would be no impact on the identification of the median employee. In fact, in some cases, even very high turnover or churn rates may have little or no impact on the identification of the median employee. Fact patterns that may contribute to changes in population that “significantly impact” the identification of the median employee include: 1) acquisitions (unless the merger exemption is to be applied) or expansions of business units that tend to be very high paying (such as research) or low paying (such as production line) relative to the median, and; 2) force reductions, which tend to skew to one end or the other.

- Has there been a significant change in the employee compensation arrangements that would significantly impact the identification of the median employee? It is uncommon for this question to be answered positively in the absence of a large influx of employees organically or by acquisition (which would trigger the question above), as broad-based compensation schemes do not significantly change year-over-year. However, if a company were to introduce a broad-based equity program where none existed the prior year, re-identification may be necessary.

Provided each of the four questions above can be answered in the negative, a company is permitted to re-use the previously identified median employee. Re-use is permitted but not required, and experience to date suggests that most companies in fact prefer to re-identify their median employee. In consulting with clients and observing developments throughout the marketplace, it appears that many companies have opted to re-identify their median employee because of the highly subjective judgments required to be made and disclosed when opting to re-use the previously identified median employee. For companies that opted in Year 2 to re-identify their median employee (for the reasons discussed above or for any other), it is likely that they will continue to do so. For companies that chose in Year 2 to re-use the previously identified median employee, there is an additional inquiry: Does the median employee, identified two years previously, remain representative? Fundamentally, the analysis is the same as above. However, because of the high subjectivity of the determinations that the company’s compensation schemes and population have not changed significantly, in many cases, the conclusion that there has been no significant change may be tenuous.

Emerging Pay Ratio-Focused Activism: Could it Change the Direction of Pay Ratio Disclosures in the Future?

Despite being a hotly contested rule, the CEO pay ratio has been a relatively quiet topic to-date. Neither proxy advisory firms or major institutional investors cite this ratio in their say-on-pay votes, policy guidelines or recommendations. That said, as with any new disclosure, there are some constituencies seeking to make use of the new information.

During the first two years of pay ratio disclosure, a coalition of pension funds and their affiliates have had a pay ratio-focused campaign, seeking supplemental pay ratio disclosures. Spearheading the campaign is a letter sent to each constituent of the S&P 500 Index and signed by 48 proponents, including New York City Comptroller Thomas DiNapoli, trustee of the New York State Common Retirement Fund (NYSCRF). The letter seeks to establish that companies’ pay ratios are an indicator of the “reasonableness of CEO pay levels,” which, the proponents argue, are useful in say-on-pay voting decisions.

In coordination with the letter-writing campaign, the NYSCRF has brought a series of shareholder proposals on companies’ ballots asking for additional information concerning pay ratio disclosure and employee pay more broadly. While these proposals have not been the subject of wide commentary, NYSCRF with co-proponents AFL-CIO Equity Index Fund and Zevin Asset Management, claims to have reached compromises with a handful of companies, which have provided — or agreed to provide — supplemental disclosures in their SEC filings and other statements.

Pay ratio-focused activism has not been known to significantly influence any say-on-pay votes and has been limited to the largest and most visible companies. It has resulted in only a handful of concessions from companies. However, we also expect proponents of this activism will continue to push for greater disclosure.

Observations Concerning Median Employee Compensation

Please note that the following results exclude Tesla due to the large CEO compensation package and pay ratio for 2018. This data point skews the overall data set and paints an unclear picture of the market when it is included.

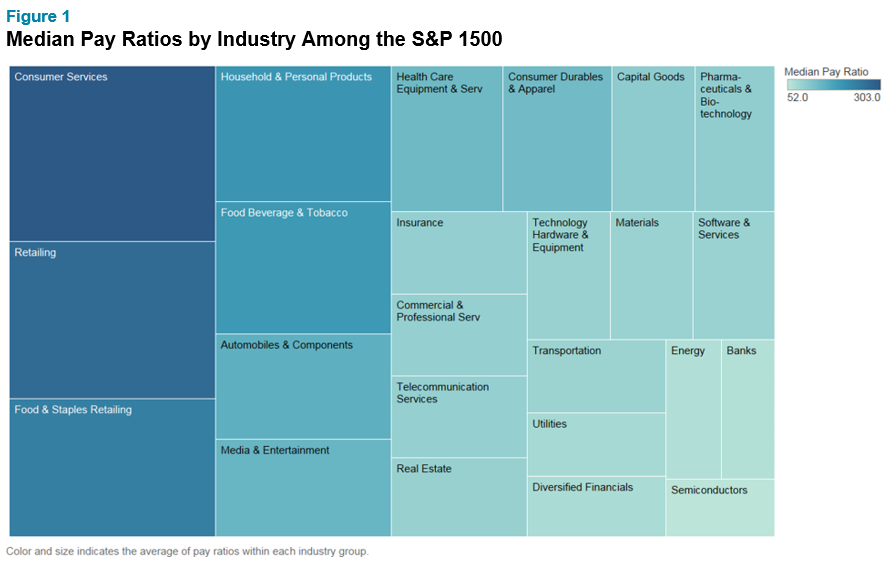

Figure 1 is an illustration of the median pay ratios by industry among the S&P 1500. The colors and size of the boxes indicate the magnitude of the median ratios compared to the other industries in the data set. We can see that consumer services has the highest median ratio value (303x) with retailing as a close second (270x). These industries have a larger number of employees who bring the median employee’s compensation downward, by including a multitude of lower-level employees (store clerks/cashiers, floor sales, etc.). Energy, banks and semiconductors (all under 70x median pay ratios) employ a larger number of highly specialized employees, thereby bringing the median compensation up and subsequently reducing the pay ratio.

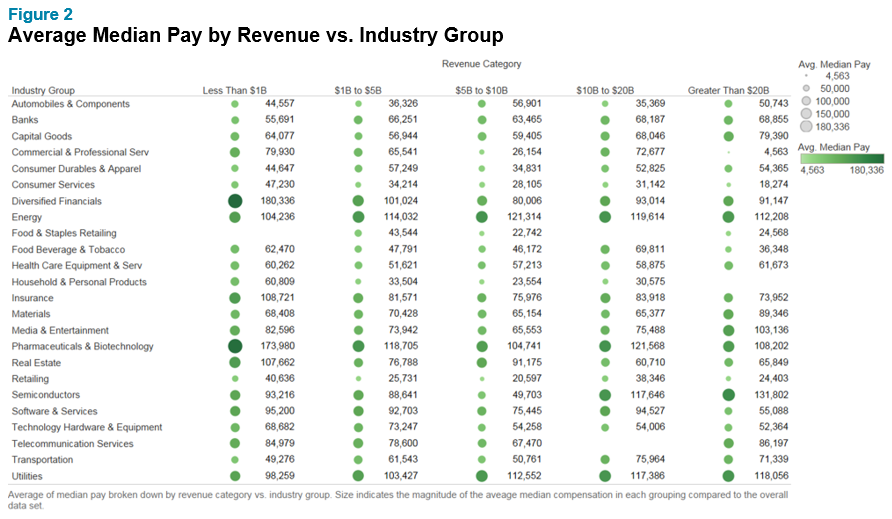

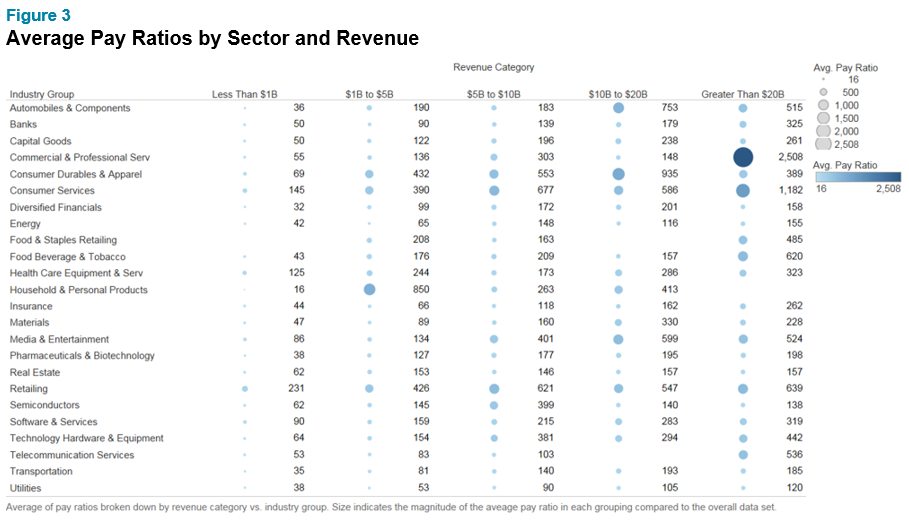

Figure 2 illustrates the average disclosed median compensation of each company in the S&P 1500 and breaks them out by industry and annual revenue for the past fiscal year. We can see that the median employee’s compensation, apart for CEO compensation, is somewhat unaffected by increases to revenue (as shown below); and generally, as revenue increases, so does the pay ratio (Figure 3 below).

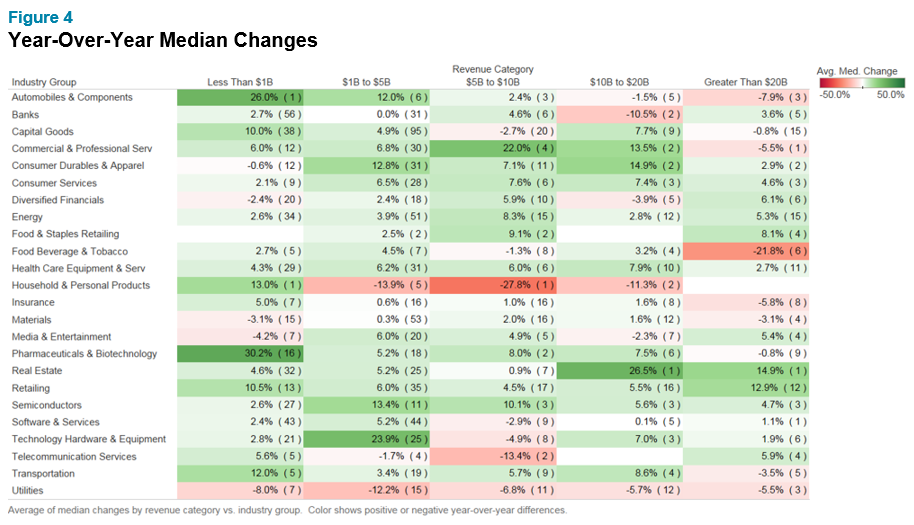

The following chart compares the change in the average pay ratio from the previous year’s disclosure for each company in the S&P 1500, and is further broken down by revenue and industry categories. Green coloring represents instances where the median compensation increased from the prior year’s disclosure, and red represents a decline. Household products and utilities had a noticable decline among all revenue groups, whereas retailing, consumer services and semiconductors experienced a consistent increase across all revenue groups.

Next Steps

If you have questions about calculating, disclosing or addressing your pay ratio and would like to speak with one of our experts, please write to rewards-solutions@aon.com.

Related Articles