Ensuring that executives are paid fairly for their performance is critical to the health of any organization. Credit unions also have a unique responsibility to their members to not pay executives excessively. In this article, we will discuss best practices for executive compensation specific to credit unions: how to determine whether your compensation meets applicable IRS guidelines and governance standards, as well as how (and how often) to compare your executive compensation to the market.

Reasonable compensation guidelines

The IRS defines “reasonable compensation” as the value that would ordinarily be paid to an individual for like services in like enterprises under like circumstances. For example, compensation for a credit union’s CEO should be comparable to CEO compensation among similarly sized organizations with similar fact patterns (industry, geography, etc.).

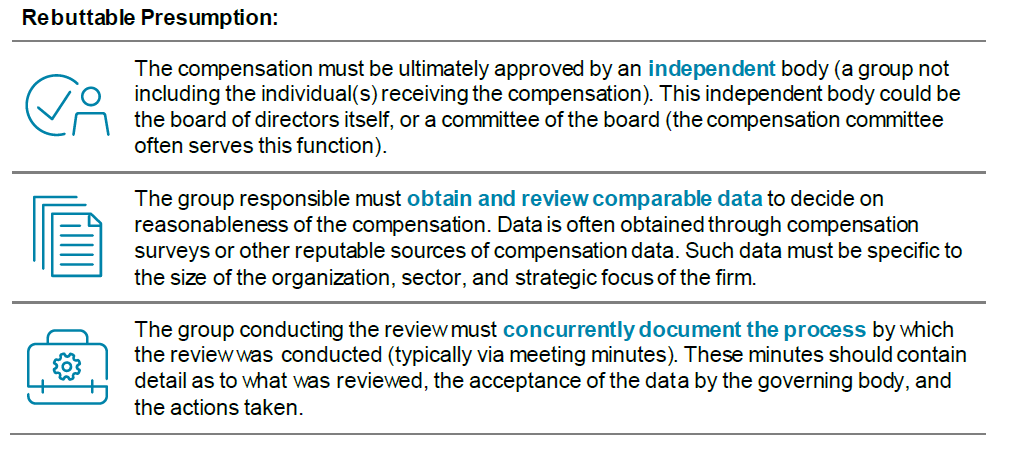

The IRS has provided a legal framework for 501(c)3 and 501(c)4 tax-exempt organizations to follow, referred to under law as a “rebuttable presumption.” Even though credit unions are not formally protected under the framework, we still recommend using this process in executive compensation governance for the following reasons:

- It is good governance practice. Perhaps not coincidentally, a governance process that satisfies the three prongs of the rebuttable presumption (outlined below) mirrors the process that many public companies use as best practice when it comes to compensation governance.

- Having solid documentation of the overall process and specific steps that informed your decision-making will strengthen your credit union’s position in the event that your executive compensation is challenged by the IRS.

- This practice supports the board’s due diligence in service to its members to confidently state that compensation provided to executives is fair and reasonable.

Credit unions should also consider the excise tax for tax-exempt organizations, which was introduced to law under the 2017 Tax Cuts and Jobs Act. The Act presented a 21% excise tax that nonprofit companies must pay when annual compensation for any of the top five most highly compensated employees exceeds $1M.

Best practices

Reviewing executive compensation need not be a daunting task. At McLagan, we specialize in helping firms tailor their executive compensation programs to the needs of the organization. Below are some recommended best practices to help credit unions review their executive compensation programs:

- Define a compensation philosophy that provides an actionable framework for decision making. Who are your competitors for talent? When it comes to employee pay, does your credit union want to lead, meet, or lag the market? What role should “at risk” compensation play in your total compensation package? What should the targeted mix of fixed versus variable pay be?

- While specific targets should be defined within your compensation philosophy, actual performance may result in compensation above or below target. This is acceptable, particularly when the philosophy has been defined, the metrics and goals have been pre-approved by the independent body, and the actual results are reviewed and approved by the same governing body.

- Select data sources that provide comparable data for your credit union.

- Use reliable data sources that include all elements of compensation (salary, cash incentives, and long-term incentives).

- Organizational complexity is usually best defined in terms of asset size or revenue, with credit unions most often using asset size. A best practice for the peer group is having a range of firms which are typically ½ to 2x the asset size of your firm, with your organization close to median.

- Normally, a peer group should be comprised of at least 16-20 firms to ensure a large enough sample size.

- Think about your competitors—who might be trying to hire your executives, and from which firm(s) would you look to hire if you had an opening? The answer could include credit unions, banks, and/or other organizations.

- Benchmark the functional role of the position when possible. For example, use peer CFO data to benchmark compensation for your own CFO. Also, for unique positions, consider benchmarking the rank order of the role, e.g., the general counsel who happens to be in the top 10 officer rank.

- Bear in mind both individual performance for your executives and the compensation philosophy of your organization when reviewing market data. There may be reasons to deviate from your stated compensation philosophy based on the facts and circumstances of the role in your organization.

- A standard executive compensation review typically includes the CEO, as well as his/her direct reports.

- Compensation for your executive team should be reviewed on an annual basis.

Key takeaway

Every organization faces the risk that its most important asset – its talented people – walks out the door at the end of each day. Credit unions face compensation challenges that simply do not exist at competitor banks, such as the inability to grant stock awards. However, by providing fair and competitive executive pay, firms can ensure that their executive talent will continue driving success and performance for the organization.

If you are interested in learning more about best practices for executive compensation and governance, please contact our team. Our consultants at McLagan are experienced in working with credit unions and can provide you the expertise needed to set your credit union on the right path.