Incorporating ESG metrics into executives’ incentive plans requires clear objectives, assessing your level of readiness and selecting elements that support business goals.

Pressure for companies to perform well in the areas of environmental, social and governance (ESG), in addition to traditional financial and shareholder measures, continues to rise. This means that accountability and transparency are critical. When assessing an organization’s performance on ESG metrics, stakeholders often first look to public filings, including a firm’s sustainability report and new required disclosure of human capital management in the 10-K. Given the momentum in this area, more companies are exploring how best to add ESG metrics to executive incentive plans.

While ESG-based incentives are becoming more prevalent, neither shareholders, regulators or shareholder advisory firms have, as of yet, made them mandatory for determining their positions relative to say-on-pay voting. This gives companies the opportunity to evaluate the incentive design that best matches their degree of readiness and how it will link to ESG-related disclosures. For some companies, especially mid- to small-cap firms, the best answer for 2022 may be to spend time improving processes to ensure full preparedness in 2023 instead of introducing ESG-based incentives right away. Conversely, companies with a mature ESG position can be more aggressive with their incentive design.

In our prior article on tying ESG metrics to executive incentives, we emphasized key considerations to assess how equipped your business is to implement ESG-based incentives. In this article, our focus shifts from laying the groundwork, to making incentive plan design choices based on your company’s level of readiness. Incentive design should start with the maturity curve and then integrate additional design factors.

Start With Assessing Where You Stand on the ESG Maturity Curve

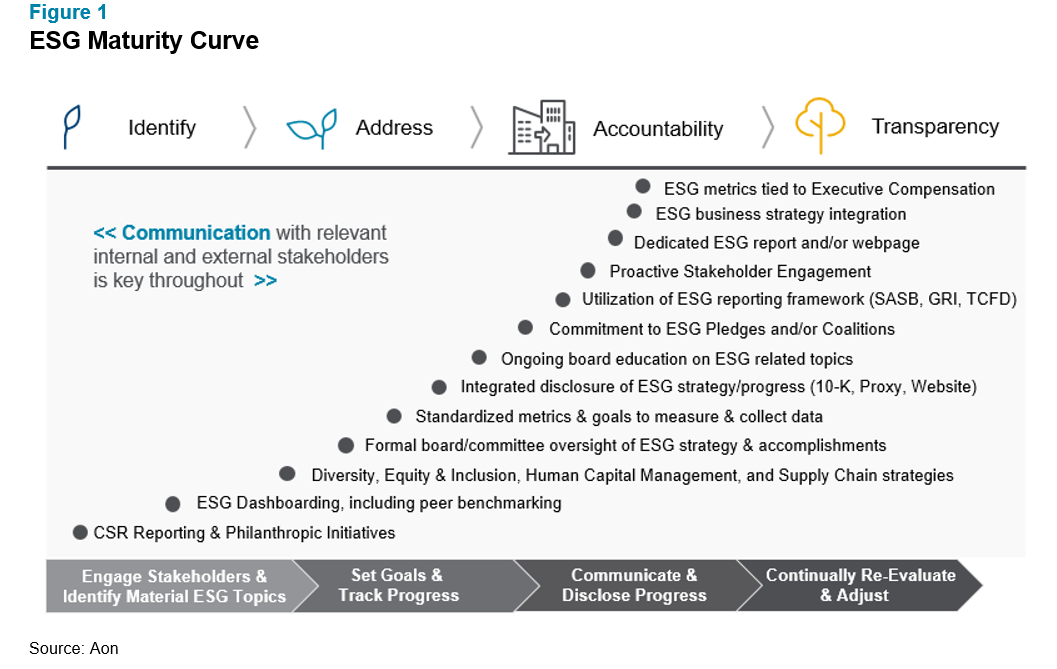

As your company matures in its approach to addressing ESG risks over time, so too, should your incentive design. Figure 1 shows the types of activities that companies will typically engage in as they move up the ESG maturity curve. The first step might be reporting sustainability initiatives publicly, while much more advanced steps include integrating ESG risk with business strategy and incorporating ESG goals into executive pay design. However, not all of these steps need to be done sequentially from bottom to top — it’s likely that your firm may have achieved some steps further along on the curve before others.

The four goals needed to meet stakeholder expectations are located across the top: identify, address, accountability and transparency. These will not be met through incentive compensation alone. We believe that ESG-based incentives are the icing on the cake, while establishing plans, processes and disclosures are the main ingredients. The four categories of activities across the bottom — engage stakeholders and identify relevant ESG topics, set goals and track progress, communicate and disclose progress, and continually adjust — summarize how to achieve the goals.

Next, Consider External and Internal Influencing Factors for Designing Incentives with ESG Metrics

External

While a key input of incentive design for the next two to three years will remain examining what other comparable companies have done over the last year, we believe this tactic to be less valuable than in the past. That’s because many companies are implementing ESG incentives for the first time while also continuing to move up the maturity curve. As those factors settle and investors, regulators and investor advisors begin to voice their opinions, we expect two to three more years before competitive practice stabilizes.

Companies should focus on a general industry comparison rather than an industry-specific one. There are likely to be some industry differences in measures chosen — for example, a manufacturing company may have a greater environmental impact than a retail company — but most design elements are industry agnostic.

So, what have companies been up to in 2020-2021? Here’s a look at what we found:

- Fifty-seven percent of the S&P 500 have included some ESG metrics in either short- or long-term incentive plans for fiscal year 2020. However, data for the Russell 3000, excluding the S&P 500, is very different. For these organizations, less than 10% of companies have included an ESG metric. This demonstrates the distinction that many larger firms have been focusing on ESG longer, and therefore are higher on the maturity curve. Even the S&P 500 data indicates that 43% of companies have not yet added an ESG metric.

- Forty percent of ESG metrics in the S&P 500 involve human capital management-related measurements, with the most prevalent in that group being diversity, equity and inclusion, followed by talent/development and turnover/retention.

- Most of the companies including ESG metrics are using them in short-term incentives.

Internal

Another factor impacting design decisions is the objectives for the incentives. These include demonstration of accountability for ESG, explaining which ESG metrics are important to both external and internal stakeholders, determining who on the board and in leadership are accountable and providing a financial incentive to achieve ESG performance commitments. While these objectives will apply across most companies, there will be some that are specific to certain firms.

Only Then, Assess Key Design Elements for Incentives Using ESG Metrics

Making smart design choices may not be as straightforward as it seems on the surface. Businesses should anticipate a one- to three-year path of progression towards an ideal state of incentive design. Here are key elements to consider along the journey.

Types of Metrics

First, let’s focus on the types of metrics. Selection criteria should include the following:

- Ability to meet accountability through disclosure

- Readiness to define and set goals

- Importance to stakeholders

- Importance to company brand

- Risks (financial or reputational)

Determining the total number of incentive metrics chosen is important as well. A company may want to include more than one metric to reflect commitment to more than one category within ESG. However, too many incentive metrics will dilute the message and motivational impact. It’s always easier to add metrics later than to eliminate.

Short-term vs. Long-term Incentives

Are your ESG targets achievable in one year or a longer term period? Typically, that is the question that would determine whether annual or long-term incentives are used. However, human capital goals (such as changing levels of workforce diversity) or sustainability efforts (such as those requiring large capital investments), could take several years to achieve. In some cases, goals may not even be achievable in the three-year time horizon of most long-term performance plans. Therefore, it may make sense to also consider short-term incentives for ESG metrics that have definable milestones that can be achieved along the way to a larger goal. Public disclosures could be used to provide context to bridging the short- and longer-term goals and their linkage to pay. Additional considerations include:

- Short-term incentives tend to have more flexibility, allowing for company designs with space for strategic and/or individual performance goals.

- Stock-based long-term incentive plans have less flexibility from an accounting standpoint. If goals are soft, including ones where the compensation committee will use judgement, the accounting may require a higher overall expense and a different pattern than ones that are hardwired as most financial and share-based goals.

Size of Target ESG Incentives

Shareholders are expecting leaders to deliver on all financial, strategic and shareholder return metrics, as well as ESG metrics. The goal is to find the proper balance between having the ESG portion of incentives large enough for stakeholders — including participating executives — to deliver meaningful reward opportunities, while also maintaining enough incentive for financial, other strategic and shareholder return performance metrics.

This is one area where looking to the competitive market should help to define reasonable parameters, even though it’s important to note that these parameters may continue to shift. From a maturity curve perspective, we believe that the higher on the maturity curve, the higher the ESG-related award opportunity can be.

Carve-Out vs. Modifier

This choice is in the same spirit of leaders being expected to deliver on all aspects of performance. Delivering on ESG metrics, but in a year the company is not delivering on financial and shareholder return metrics, should not result in a significant total incentive award. The choice of carve-out versus a modifier should be closely tied to the targeted incentive level. In general, a small percentage of the total (5%‒15%) will work as a carve-out.

For larger amounts, we believe serious consideration should be given to a modifier; then the total ESG dollars earned will align with the financial/shareholder return performance delivered.

Eligibility

The most visible group is the Named Executive Officers (NEOs), which we expect to have the minimum level of participation. Eligibility should include any executive with a material ability to impact the chosen metric. For some human capital measures, companies may want to shift down to the hiring manager level. The first year could be a time to start with a smaller group and let it grow naturally. Alternately, firms looking to quickly affect change can start big. In many cases, broader change management considerations are just as important as incentive design.

As more data on plan design choices becomes available, we will learn how shareholders and shareholder advisors react to the current schemes. As stated earlier, we expect the next two to three years to be ones of adjustments as companies move along the maturity curve and more frequently include ESG metrics within their incentive plans.

Next Steps

Including ESG metrics in executive incentives is a trend that’s here to stay. While many firms have only recently adopted ESG incentive metrics or are in early stages of consideration or adoption, it is becoming necessary to create a plan for implementation and how the incentive design may shift over time. It’s important not to rush the process. Using ESG-based incentive compensation demonstrates greater accountability, but it also magnifies risk. From a risk management perspective, there are a few key reputational risks to consider, including:

- Shareholders judging the goals not rigorous enough for the company;

- An increased risk of lawsuits. This has already occurred with companies using DE&I metrics who did not achieve the stated goals. The potential for legal liability related to other measures is unknown. While we do not expect this to stop companies from using ESG metrics in incentive compensation, the risk should be monitored; and

- Unachieved ESG goals affects constituencies beyond shareholders, including judgements from the community and your employees.

The time for ESG-based incentive compensation is now. Make sure to weigh all your options and get it done right. For whatever stage of the readiness curve you are on, Aon is here to help. To learn how we work with firms on their ESG strategies, including corporate disclosure and executive compensation design, please visit our future-ready boardroom hub. You can also read our previously published article, A Framework for Tying ESG Metrics to Executive Compensation Plans, which shares insights for laying the initial groundwork to ensure you are prepared to dive into the incentive plan design elements and choices we consider in this article.

If you have questions and want to speak with one of our experts, please write to rewards-solutions@aon.com.