Our research into the second year of required human capital management disclosure in companies’ Form 10-Ks finds a continued general lack of quantitative information. However, within the most prevalent topics for disclosure, we are observing more data being included, particularly when it comes to diversity, equity and inclusion.

Public companies in the United States (U.S.) have completed the second year of required disclosure regarding human capital management (HCM), allowing stakeholders to compare year-over-year changes in how companies are disclosing HCM and different topics of interest.

To see how this disclosure is evolving, we analyzed 496 filings from S&P 500 companies for the 2021 fiscal year and compared to the prior year. The most common topics covered by companies are largely the same as the first year of the disclosure rule (see our analysis of year one disclosures here). However, individual companies are disclosing more details on these topics, leading to more robust disclosures.

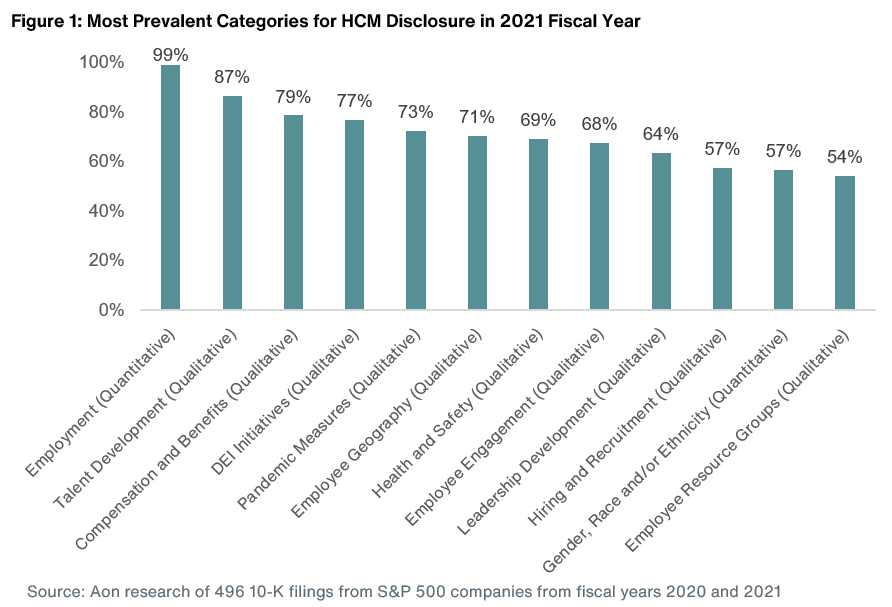

In this article, we explore year-over-year changes in disclosure, hot topics being addressed, and how companies can prepare to meet stakeholder expectations for HCM disclosures in the future. The chart below illustrates the most common categories in year two of the required disclosure.

How Year Two Disclosure Compares to Year One

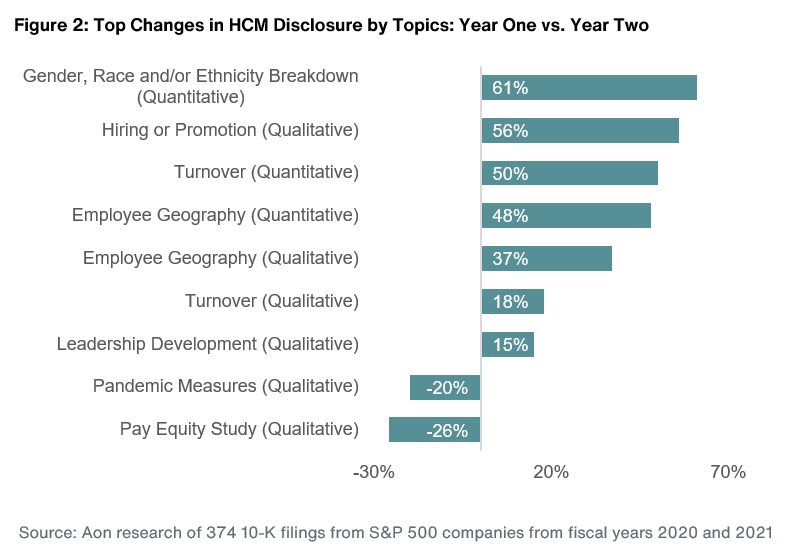

While the categories of these disclosures have not changed meaningfully in this second year, S&P 500 companies are including a broader set of topics and more in-depth information. We looked at a subset of 374 companies in the S&P 500 to analyze how their year-over-year disclosures have evolved. The results in Figure 2 show the nine categories where we saw a greater than 10 percent increase or decrease in disclosure across the same sample of companies.

The category with the most additional information added is gender or race/ethnicity breakdown. Companies disclosing this quantitative data increased by 61 percent in year two compared to year one. We also saw an increase in disclosure related to talent attraction and retention — a hot topic many companies are currently challenged with. Consider the following year-over-year changes:

- 56 percent increase in hiring or promotion disclosures

- 50 percent increase in data on employee turnover

- 48 percent increase in quantitative data on employee geography, such as the number of employees by country or region

- 15 percent increase in leadership development disclosures

However, quantitative turnover was still reported by less than 20 percent of the subset of the 374 companies.

In some cases, companies reduced the amount of disclosure. There was a 26 percent drop in pay equity study disclosures and a 20 percent decline in discussions on pandemic measures. The drop in pay equity study disclosures may indicate that companies are acting on the results that came out of the flood of pay equity audits conducted in 2020, rather than focusing discussion on the audits themselves. Going forward, we may see a cyclical pattern with a surge in pay equity discussions tied to headline pressures and companies’ periodic pay gap analyses.

The increase in topics covered by individual companies may be a move to get in front of additional human capital disclosure requirements in anticipation of potential forthcoming rules that may be issued by the SEC. Chairman Gary Gensler stated in August 2021 that he asked the SEC staff to propose recommendations for enhanced HCM metric disclosures beyond the number of employees, such as workforce turnover, skills and development training, compensation, benefits, workforce demographics including diversity, and health and safety.

“As the SEC rule is principles-based disclosure, we expect the types of information provided by companies to continue to be refined over the coming years,” says Pamela Greene, Aon’s head of North America Corporate Governance and ESG Advisory group. “Just as we have seen an evolution within Compensation Discussion & Analysis disclosures over the last 15 years, we expect human capital disclosures to similarly progress in their structure, issue-coverage and depth over time, reflecting dynamic investor expectations,” she says.

Key Themes From Year Two Disclosures

The increase in topics and quantitative metrics covered by individual companies may also help convince the SEC it’s not necessary to revise the rule to make it more formulaic and require specific human capital metrics to be disclosed. SEC Chairman Gary Gensler stated in August 2021 that he asked the SEC staff to propose recommendations for enhanced HCM metric disclosures beyond the number of employees, such as workforce turnover, skills and development training, compensation, benefits, workforce demographics including diversity, and health and safety.

“As the SEC rule is principles-based disclosure, we expect the types of information provided by companies to continue to be refined over the coming years,” says Pamela Greene, head of Aon’s North America Corporate Governance and ESG Advisory group. “Just as we have seen an evolution within Compensation Discussion & Analysis disclosures over the last 15 years, we expect human capital disclosures to similarly progress in their structure, coverage of issues and depth over time. This all reflects dynamic investor expectations,” she says.

Key Themes From Year Two Disclosures

Most of the S&P 500 companies begin their year two disclosures with a workforce overview, with 99 percent including data on the size of their workforce and 71 percent providing details on their geographic footprint. Following this information, nearly half of companies provide a statement on the existence of collective bargaining agreements (CBAs). Of the companies subject to CBAs, 58 percent provide quantitative data such as number of CBAs or number of employees covered by them.

Topics of disclosure can be largely grouped into four categories. These include hiring and retaining talent; diversity, equity and inclusion; employee engagement; and COVID-19, health and safety.

We explore each of these sections in more detail below to provide trends on HCM actions and disclosures to help organizations consider for next year the level of disclosure around their HCM strategy.

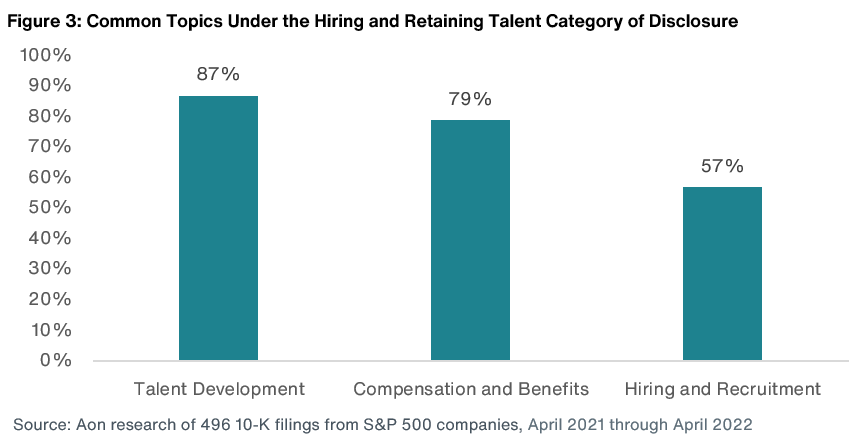

Hiring and Retaining Talent

The majority of companies address the current competitive job market by highlighting their hiring and talent development strategies: Fifty-seven percent of companies discussed recruitment and hiring, with 21 percent of those companies including quantitative data predominantly around new-hire statistics.

Similar to the first year of disclosure, talent and leadership development was an area of focus, with 87 percent of companies covering this topic. Companies discussed training and mentorship programs, including data on participation rates.

In addition to employee development, 79 percent of companies discussed the competitiveness of their compensation and benefits as part of their hiring and retention strategy. Some companies discussed the shift in their benefit programs to address the effects of the pandemic on their workforce, such as the expansion of mental health and wellness benefits.

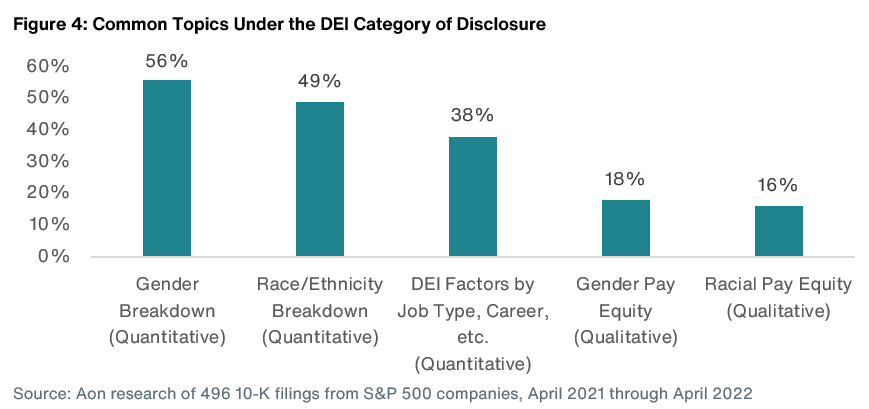

Diversity, Equity and Inclusion (DEI)

Most companies discussed DEI in their human capital management disclosure. Seventy-seven percent discussed specific DEI initiatives, such as unconscious bias training, diverse candidate recruitment and employee resource groups.

We also saw an increase in quantitative DEI disclosures compared to the prior year, with 56 percent disclosing the gender breakdown and 49 percent disclosing the race/ethnicity composition of their workforce. In addition, 38 percent of companies overlay these quantitative diversity metrics with job type, career levels and other categories, which presents a more in-depth look at their workforce diversity.

As mentioned, we did see a decline in disclosure of pay equity studies from the prior year. Only 18 percent of companies mentioned conducting gender or race/ethnicity pay equity studies, and 31 percent of those include quantitative data. Examples of this include the percentage of pay disparity and cents on the dollar earned by women or people of color compared to men or non-minority employees.

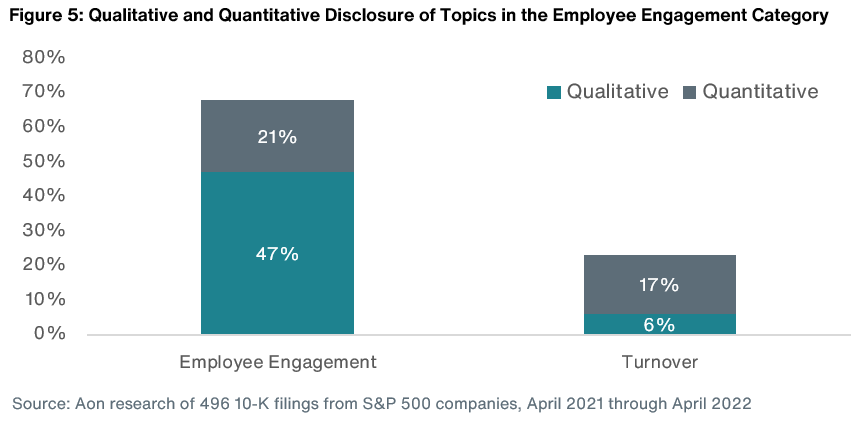

Employee Engagement

Employee engagement was a popular topic in this second year of disclosure, with 68 percent discussing it. Of that group, 31 percent included quantitative metrics, such as participation rates in pulse surveys or the results of those surveys. Employee resource groups were discussed in 54 percent of disclosures, which often intersected with DEI initiatives. Employee turnover — an important indicator of employee engagement — was mentioned by nearly a quarter of companies.

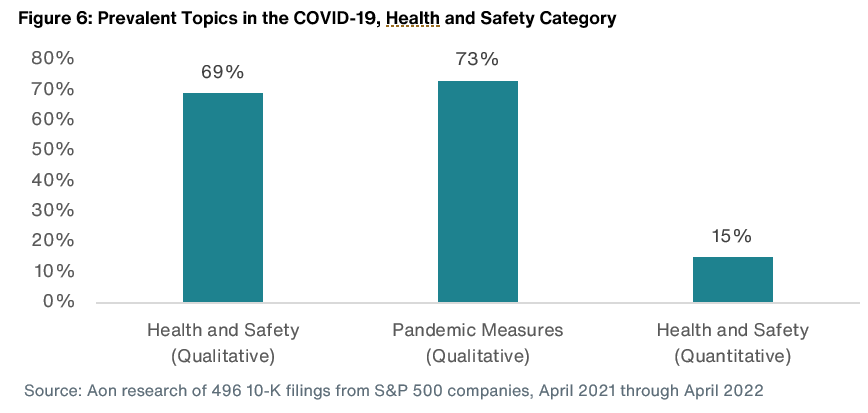

COVID-19, Health and Safety

Although there was a year-over-year decline in COVID-19 coverage, pandemic measures continued to be a prevalent topic, with nearly three-quarters of our sample companies providing disclosure. The pandemic was often mentioned as part of location strategies and protocols. Sixty-nine percent of companies discussed the health and safety of their workforces, including mental health and wellbeing. Of those that covered health and safety, 22 percent included quantitative data such as injury rates in their disclosure.

Staying Current on Hot Topics in Disclosure

The four key themes discussed above represent topics that most organizations believe to be material. If your human capital management disclosure does not include these topics, consider adding this information in next year’s Form 10-K to align with general market practice.

It is also important to monitor topics that have begun to gain significant traction, such as disclosing quantitative DEI factors by job type or career, discussing pay equity studies and addressing turnover. This information may become more commonplace next year. Companies can prepare now by gathering this information and presenting it to the full board or a board committee so they can be apprised of these metrics and understand the year-over-year changes and reasons for it.

In addition to these key themes, there are other sector or company-specific issues that may be relevant to include as well. Looking to industry peer practices can help ensure company disclosures are aligned with the market on issues and metrics.

Next Steps

Put simply, investors, proxy advisors and employees want to see more detailed and quantitative human capital management disclosures. When addressing these topics, companies should consider the following:

- Provide detail that demonstrates the depth of your HCM strategy to best meet stakeholder expectations.

- Include information on leadership responsibility, relevant programs, established publicly disclosed goals and targets (including employee engagement scores, pay equity and diversity), as well as recognitions and metrics.

- For calendar year-end companies, begin thinking about revisions to your 2023 HCM disclosure now rather than waiting until the end of 2022 or the start of 2023.

- Consider peer benchmarking to identify any gaps in your disclosure and needed policy updates in light of changes in the business environment over the past year. For example, determine whether COVID-19 safety measures and pandemic-era employee benefits should be omitted from the 2023 disclosure. Likewise, consider whether the adoption of a hybrid or virtual work model or benefits to stave off the high employee turnover should be added to the disclosure.

- Keep in mind that the company will need to review the proposed disclosures with the board committee responsible for human capital oversight. Build in time for this review so the company can consider and incorporate feedback well in advance of next year’s 10-K filing deadline.

If you have questions about your human capital disclosure and strategy or how your disclosure compares to your peers, please contact one of the authors or write to humancapital@aon.com.