The SEC’s proposed climate disclosure rule would bring the U.S. more in line with other regulations globally. Whatever form the final rule takes, companies should prepare now for new and more in-depth climate disclosures and growing expectations from stakeholders.

When the United States (U.S.) Securities and Exchange Commission (SEC) proposed new disclosure rules in March 2022 that will transform the landscape of climate reporting, many companies were already expecting more comprehensive emissions disclosure based on recent regulatory action in other parts of the world. Whatever form the final rule takes, it’s clear that enhanced disclosure is coming to the U.S., and companies need to prepare.

In its current form, the proposal would require all publicly traded companies to disclose their greenhouse gas (GHG) emissions in a standardized fashion and the risks they face from climate change. Creating a more standard reporting system for emissions would follow a trend of similar disclosure requirements in other countries.

In the United Kingdom and Japan, for example, certain large companies must disclose GHG emissions starting this year. The European Union will require publicly traded companies to disclose GHG emissions by 2024. Brazil, Hong Kong, New Zealand, Singapore and Switzerland will also soon require mandatory climate risk reporting. As a result of this increased complexity of climate-related disclosure rules globally, companies will need to consider implementing processes and procedures for monitoring and publicly reporting climate risks, governance oversight, emissions and more.

What the SEC proposal entails

While the proposed rules in the U.S. are not final and are likely to go through changes based on the significant amount of comments, the proposal would require public companies to disclose information about the following:

- Company board and management oversight of climate-related risks

- Impact of climate-related risks on business and financial statements (past and future), as well as a related requirement to disclose the impact of climate-related events and transition costs

- Impact of climate-related risks on company’s business strategy (past and future)

- Processes for identifying and addressing climate-related risks, and strategy for integrating climate-related risks into overall risk management strategy

- Transition plans relating to climate-risk management strategy

- Scenario analyses used to assess business resilience to climate-related risks

- Information about internal carbon prices, if applicable

- Information about the scope, timeline, strategy, and metrics of any publicly set climate-related goals

- Scope 1 and 2 emissions metrics, including an attestation report covering Scope 1 and 2 disclosures; Scope 3 emissions if material or included in a firm’s targets or goals

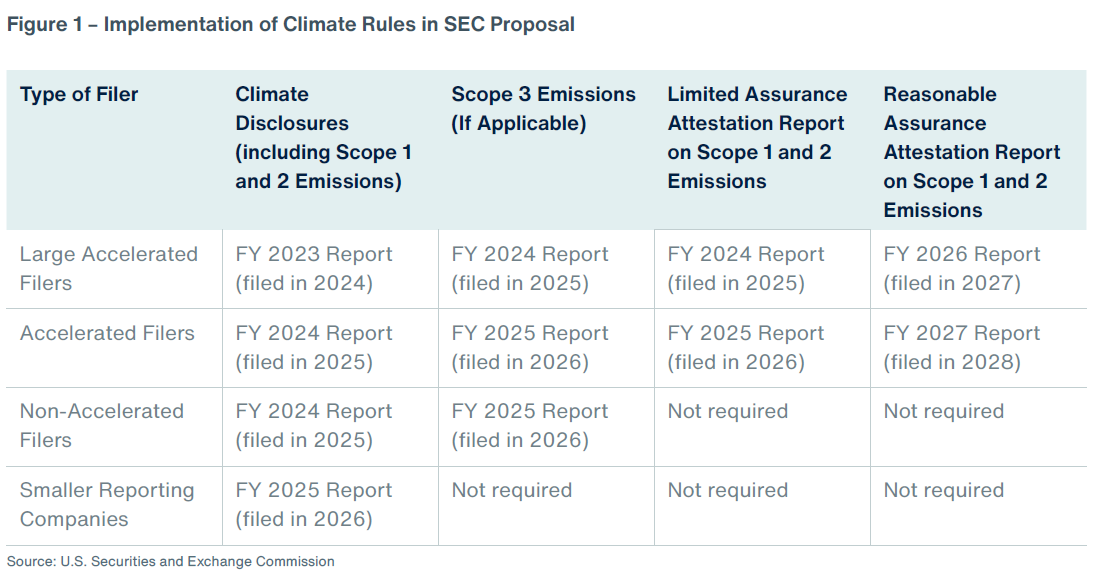

The SEC extended the comment period for the proposal to June 17, 2022, and around 6,000 comments were submitted — the most the agency has received on a proposal. The agency said it expects the final rules to be effective by December 2022 and proposes the following implementation dates:

The opportunity to act now — and the risks of not doing so

The proposed regulations represent a milestone in the environmental, social and governance (ESG) movement. Investors and other stakeholders want to know how companies are addressing their climate risks and are increasingly asking for more standard disclosure around emissions reporting. Companies that don’t start preparing now risk falling behind their competitors, alienating stakeholders, potentially shutting themselves off to new forms of capital, exposing themselves to reputational risk, and scrambling to comply when new rules are finalized.

On the upside, taking a proactive and thoughtful approach to climate strategy can result in a broad range of benefits, including:

- An enhanced reputation for a healthy dialogue with customers and investors

- Improved access to capital

- A business model that enables and supports long-term resilience

- A more attractive workplace for talent

- An improved risk management process and overall enterprise risk framework

While the rules aren’t final, the sooner businesses begin assembling information related to the proposal and ensuring they are prepared, they will be better positioned to comply quickly. We recommend companies incorporate the following questions as they prepare for future regulation:

- Determine Oversight. Who has oversight and responsibility for climate-related risks and opportunities within management? Is this information reported to the board of directors (or a key committee tasked with ownership of this topic)? What governing policies and procedures are in place for oversight and responsibility within management and the board?

- Upskill the board. Board members are finding themselves in need of more information and education on ESG topics including climate. Management should consider whether and to what extent to provide the board regular updates on the company’s climate strategy, tailored trends and education. Ensure public disclosure on how the board is receives this information.

- Assess Climate Risks and Opportunities. Identify, quantify and assess the ways climate change will impact the company. Both physical and transition risks must be considered; scenario analysis is the most commonly preferred method to undertaking an assessment.

- Verify Climate Metrics. What climate-related information is currently tracked, measured and monitored and/or reported? Is such data reviewed by a third-party for verification or assurance?

- Understand Global Frameworks. Take steps to understand the commonly recognized disclosure frameworks that exist. The Task Force on Climate Related Financial Disclosures (TCFD) is one of the most recognized frameworks and recommends disclosing a company’s efforts around both climate action and resilience plans. To learn more, see our article “Early Adoption of Climate Disclosure Frameworks: The Benefits and Challenges.”

- Evaluate Climate Commitments. What climate-related public statements, claims or commitments have been made by the company? Does the company have a way of tracking or coordinating such information across departments?

- Gauge Materiality. How do you define materiality for climate-related risk? It may be necessary to integrate climate disclosures and processes with the SEC and financial reporting disclosure processes.

The proposal will impact industries differently

The proposed regulations apply to all publicly traded companies in the U.S., but the impact will vary depending on a company’s industry, unique environmental footprint and how far along a company is in addressing and disclosing emissions.

- Financial Services: Emissions financed by banks (considered Scope 3) place a potentially more onerous burden for the industry. Firms with more than $700 million in market cap would be considered large accelerated filers and would have to meet requirements in a more compressed timeline. This threshold would capture approximately 150 of the largest publicly filed banks.

- The rule is also intended to elicit disclosure around the range of climate scenario analysis undertaken by banks, as well as financial metrics outlining balance sheet exposure or risk to climate change (inclusive of banks’ corporate footprints and loan portfolios). The starting point is building new models to help quantify exposure to physical and transition risk across both operational portfolios and lending portfolios. As financial institutions begin to do this, it will improve their disclosures and ultimately enable more informed risk management approaches.

- Energy: Given their environmental impact and potentially significant role in transitioning to greener energy, the pressure on energy companies from all stakeholders, including shareholder activists, will likely increase. Last year there were a handful of campaigns from activist funds to unseat board members and approve new types of resolutions to disclose emissions data that were successful.

- Food, Agriculture and Beverage: The future of the food, agriculture and beverage (FAB) industry will be influenced and financed by multiple stakeholders, including consumers, regulators, governments and investors. While the proposed SEC rules apply to publicly traded companies listed in the U.S., it’s likely that external stakeholder pressure will encourage privately held and foreign owned FAB companies to comply as well. Leaders and innovators in the industry have been proactive around voluntary climate disclosures in line with TCFD recommendations, with a shift in mindset beyond simply profit to a “people-purpose-planet” agenda.

- Dairy and meat businesses will be particularly challenged navigating the emission disclosures given their volume of methane emissions. While many FAB companies have made progress in identifying physical and transition risk, our clients are leveraging the power of predictive analytics to better understand, quantify and model this risk, with a view to informing the business strategy on climate and ensuring the issue is core to the enterprise risk framework.

Disclosure involves long-term planning

While the SEC proposal focuses on the way organizations plan for and disclose their approach to climate change, having a plan to disclose is only the start. Climate disclosure tends to be a multi-year investment for most organizations.

The journey should begin by understanding the current baseline of climate regulations and actions expected, reflecting on the climate-friendly activities already undertaken within your business, address ongoing efforts, and finally project climate-related plans for the future.

As we have learned from other global regulations, investors and regulators will be looking for organizations to make progress on their climate-action plans and efforts related to risk and resilience. Organizations will need to assess the impact of transition to net zero and the implications of climate change (risks and opportunities) in both the near and long-term and build climate resilience plans. These activities should be front of mind for in-house risk management and sustainability teams, but the nature of climate change means assessing the implications may not be as straightforward as the ways they assess present-day risk.

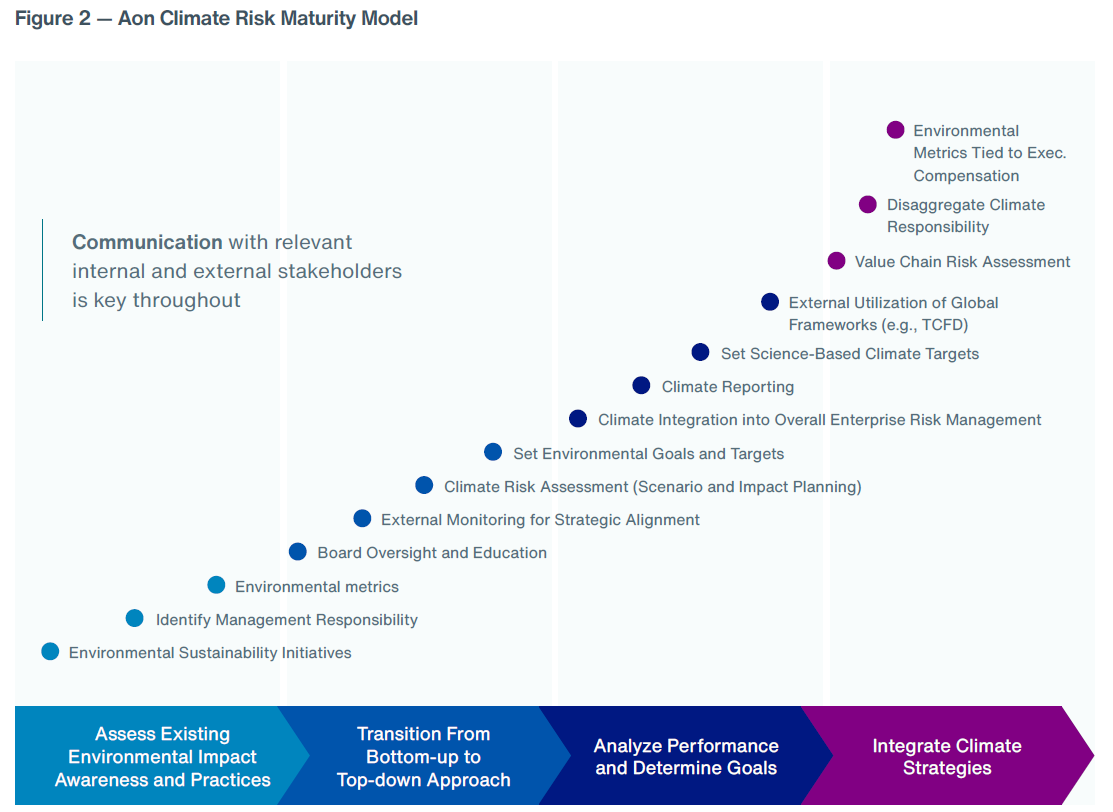

Aon is assisting clients around the impact of transition to net zero and the implications of climate change. Our climate maturity curve outlines the steps on a journey to address climate-related risks and opportunities.

Aon’s team of climate, risk and ESG experts offers independent advisory services and world-class data and analytics capabilities on climate risk, reporting and governance. We support clients on their climate strategy in three primary ways:

- accelerating the transition to net zero emissions by attracting new forms of capital,

- building physical resilience through tools such as our Climate Change Risk Assessment, which addresses the risks of climate change on a company’s physical assets while modeling transition hazards that will have the most impact on a company’s portfolio, and

- reducing volatility by identifying implications of climate scenarios across all areas of a business through Aon's climate sustainability risk and opportunity identification process.