More technology employees are approaching retirement and asking whether they have to forfeit unvested shares. For companies, the decision isn't an easy one.

The wave of technology companies that went public in the 1990s are beginning to deal with an aging workforce—presenting a new set of issues that many companies have not yet previously had to address around retirement plans. One of these issues being raised more frequently by employees approaching retirement age is whether they will be able to take their unvested equity with them when they retire. The decision for employers to accelerate equity vesting isn't one to take lightly: a host of technical plan administration questions apply, including retirement eligibility requirements and corporate tax obligations.

When many technology-oriented companies were putting retirement plans and policies in place years ago, the question of what happens with unvested equity wasn't a primary concern. Most of these firms didn't have many employees near retirement age. More mature technology companies hadn't relied as heavily on employee equity compensation and, therefore, weren't as concerned with unvested equity. Fast forward to the present day, and employees approaching retirement age are naturally getting more serious about their retirement planning, and asking their employers what will happen to their unvested shares.

In our consulting and survey advisory practices, we have received more frequent questions from our clients asking what their peers are doing in this area. To take a closer examination, we recently surveyed 28 technology-related companies, largely based in the US, on their equity practices pertaining to retirement (please see the index for a breakdown on the size, industry and location of the companies polled). The results show equity acceleration upon retirement is still not very common, but there are signs some companies are at least contemplating potential changes in this area. This is no doubt linked to an increase in retirement-eligible employees.

A Rare Practice Revisited

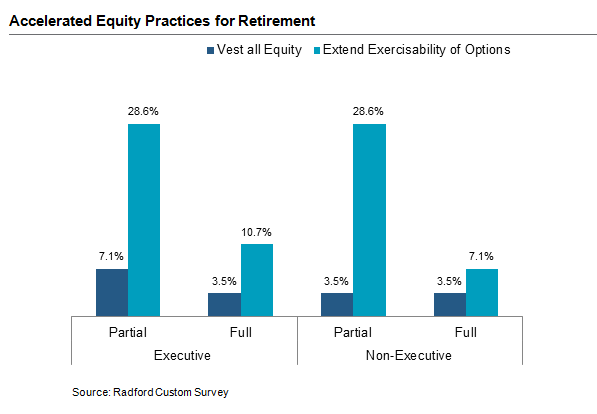

Unlike severance and change-in-control provisions, retirement plans tend to be a company-wide policy. The results of our custom survey on equity practices support this notion. While a minority of companies provided full or partial vesting of unexercised options or unvested restricted stock, the few that did were likely to offer this benefit to both their executives and broad-based employees.

Very few companies studied provide for any acceleration of vesting. If anything, it is more common for companies to freeze the vesting upon retirement, but allow the stock options already vested a longer period to exercise than the typical 90 days provided for other forms of employment termination. A little over a quarter of companies provide for some fixed extended period of time to exercise while far fewer extend exercisability all the way to the end of the option's original contractual term.

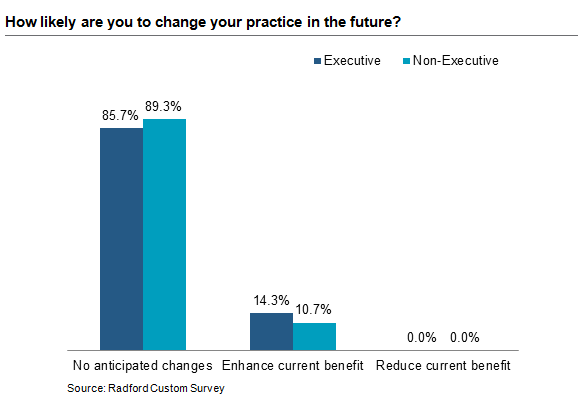

As evidenced by the next chart, most companies aren't planning to make changes to their executive and non-executive equity acceleration retirement policies. However, a meaningful minority of companies said they are planning to increase their current benefits. No companies said they plan to reduce benefits.

On top of the 10% to 15% of companies that anticipate enhancing benefits, there were additional participants that acknowledged a need to address this issue at some point in the future. “We believe that as our company matures, we will address retirement eligibility and disability/death benefits. At this time, there has not been an urgent request from employees to add these features to our plan,” said one participant at a large, US technology company. Several respondents said their company's decision to accelerate equity is not written into their retirement plans, but is an ad hoc decision based on a variety of factors. “For retirement vesting, it depends on the age and length of service of the retiree whether some of the vesting is accelerated for some or all of the grants,” wrote an executive compensation manager at a US-based technology company.

Next Steps

If your organization is considering adopting a policy to accelerate employees' unvested equity upon retirement, one of the first decisions to make is determining eligibility. Should you offer this benefit to all employees that receive equity as a form of compensation, or reserve eligibility for higher job levels? As the first chart illustrates, most companies we surveyed that offer accelerated equity benefits provided this to all of their employees that receive equity. An organization's equity culture and retirement plan practices will factor into that decision. A second eligibility consideration is defining retirement. Since most technology companies don't offer pension plans, which carry strict retirement requirements, some firms may want to revisit their retirement plan eligibility if they are considering extending benefits to include accelerated equity.

Another major consideration is the accounting expenses both employers and employees will assume by accelerating equity. ASC Topic 718 requires companies that allow vesting acceleration to recognize the expense from the date of grant to the date the employee becomes eligible to retire— regardless of whether or not the employee actually retires when he or she is eligible to. This could mean 100% of the expense is recognized on the date of grant if the employee is already eligible. If there is no accelerated vesting, the company would amortize the cost over the full vesting period of the shares. The thinking behind the regulation was that accelerating equity eliminates the risk that any shares will be forfeited when an employee reaches retirement eligibility. In practice, however, it has added a potential expense to employers.

While the practice to accelerate equity is not widespread, more companies are considering the merits of adopting such a practice. It's not a clear-cut decision. The benefits to employees may seem obvious, but the added administrative burden and potential for accelerated expense recognition are definite downsides the company experiences.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to [email protected].

Related Articles