The influence of ESPP design on valuation

Introduction

Companies’ Employee Stock Purchase Plans (ESPPs) can have myriad structures and features. There is considerable variability with regards to the length of the purchase period, the discount being offered (if any), a share match (utilized in some non-qualified designs), and the inclusion of a look-back feature. Additionally, ESPPs can be either tax-qualified (Section 423 plans) or non-tax qualified. The fair value of an ESPP depends on both the structure of the plan and the economic assumptions used in the valuation model.

A fair value must be determined for ESPPs when they are deemed to be “compensatory.” And most ESPPs are considered compensatory as a result of having either a look-back feature or a discount greater than 5%. In this article, we will describe the basics of ESPP valuation, walk through some valuation examples, and examine some of the accounting challenges for certain types of ESPPs.

The Basics of Valuing ESPPs

For a typical ESPP, employees withhold either a fixed dollar amount or a stated percentage of the employee's salary over a specified period to purchase stock. One of the most common ESPP designs offers employees the opportunity to purchase shares at a discount (usually 5%, 10% or 15%) from whichever is lower: the market price at the beginning of the offering period or the market price on the date the purchase is made. Plans with this design are known as a look-back feature since the purchase price is using the lesser of the grant date or purchase date stock price. From an accounting standpoint, these plans are said to have “option-like” features that provide participants variable payouts depending on how the market price moves over the offering period. The accounting standard requires these types of ESPPs be accounted for in a specific way, considering the value of the stock option-like features.

Specifically, the fair value of an ESPP is calculated as a sum of components, depending on the features of the plan. The valuation method is unique compared to employee stock options, which are valued as one component using a Black-Scholes or lattice model. This is because the potential value delivered to ESPP participants is very different compared to an option. An option only delivers value to award holders when the value of the stock increases over the exercise price, while an ESPP with a look-back and a discount delivers value to an award holder whether the stock price stays the same, declines or increases.

The inputs and assumptions used to determine the fair value of an ESPP are listed below:

Offering Date Stock Price: The price on the first day of the offering, which is generally the closing stock price, as described in the plan document. Common variations include the closing price on the trading day prior to the offering date or the average of the high and low stock prices on the offering date.

- Grant Date Stock Price: This is typically the same as the Offering Date Stock Price, but could vary under certain circumstances, such as a plan not being approved by shareholders by the offering date.

- Expected Life: This is the length of time from the grant date to the purchase date. Longer purchase periods result in higher fair values.

- Volatility: Generally, the expected volatility is based on implied volatility, historical volatility, or a combination of the two, calculated commensurate with the expected life. This should be consistent with the methodology used to calculated volatility for other employee equity, such as stock options. Similar to options, companies with higher volatilities have higher ESPP fair values.

- Risk-Free Rate: This is based on the United States Treasury rate commensurate with the expected life of the options. Higher risk-free rates result in higher ESPP fair values.

- Dividend Yield: The dividend yield is based on the company’s expected dividend yield over the Purchase Period. Increases in dividend yields result in lower fair values — similar to stock options.

Calculating the fair value of an ESPP share requires the examination of several inputs, similar to stock options, including grant date stock price, expected life, volatility, risk-free interest rate, and dividend yield. The assumptions are determined as of the grant date, which usually coincides with the first day of the offering period.

Valuation Examples

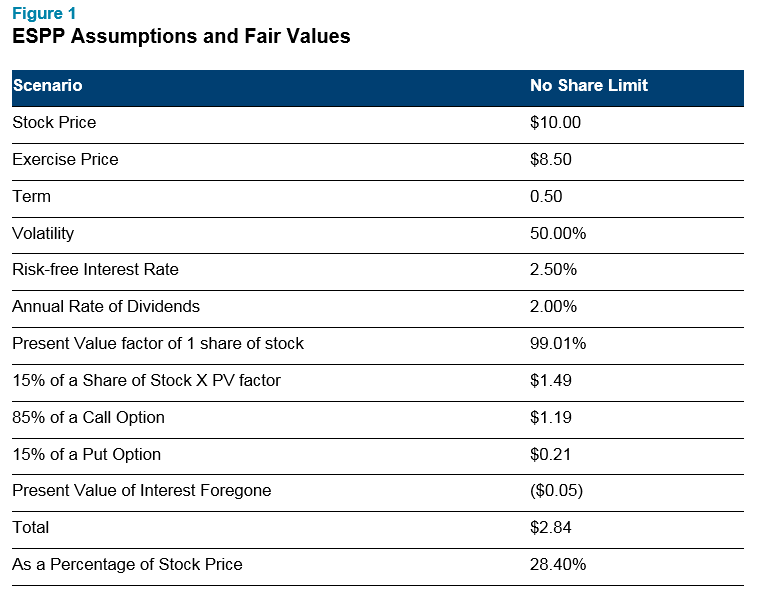

The most common type of ESPP has a six-month offering period, a 15% discount, a look-back, and allows employees to purchase as many shares as the full amount of the employee's withholdings will permit, within certain IRS and company-specific limitations. The accounting rules specify how to estimate the fair value for this type of ESPP as a sum of four components, outlined below.

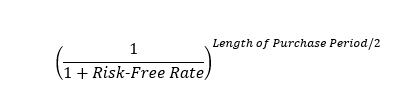

- 15% of a share of stock: This component represents the value delivered from the discount. The value of a share of stock should also consider a present value factor if there are dividend payments made to shareholders that ESPP participants do not participate in. The formula below illustrates the calculation of the present value factor. As illustrated in the equation below, if the dividend yield is 0%, the present value is 1, and the first component would simply be the discount multiplied by the grant date stock price.

- 85% of a call option: This component represents the potential benefit if the stock price increases from the beginning to the end of the purchase period. The percentage is determined by calculating 100% minus the discount the ESPP provides.

- 15% of a put option: This component represents the guaranteed discount if the stock price decreases and participants can purchase additional shares. It is essentially a protective put embedded in the ESPP that preserves the total value of an employee’s investment. This percentage is determined by the discount the ESPP provides. We note that the value of the put option can be reduced or even zero if a participant reaches a limit set either by the IRS of the plan itself. (Please see our article Are You Taking Too Much ESPP Expense? for more details on calculating the fair value of an ESPP with a share or price limit.)

- Interest forgone: This represents a reduction in the fair value for the effect of foregone interest for ESPPs that do not pay interest on contributions collected over the purchase period.

Depending on the design features of the ESPP, you could include different combinations of the above components when calculating the fair value. For example, another common ESPP design is to offer a discount but no look-back feature. That fair value is based on the first and fourth components, which are the discount and the interest foregone.

Additionally, some companies include a sales restriction after purchase, which means participants cannot sell their shares for a specified amount of time (usually from three months to one year). About 22% of qualified plans and 31% of non-qualified plans include this provision, according to the 2017 NASPP Stock Plan Survey. The primary reason a company includes this feature is to promote longer-term share ownership, as opposed to the ability to sell shares immediately upon purchase. However, employees perceive holding periods as riskier and tend to participate less frequently and contribute at lower levels. A mandatory holding period may be considered in the fair value estimation for an ESPP, which will lower the compensation expense.

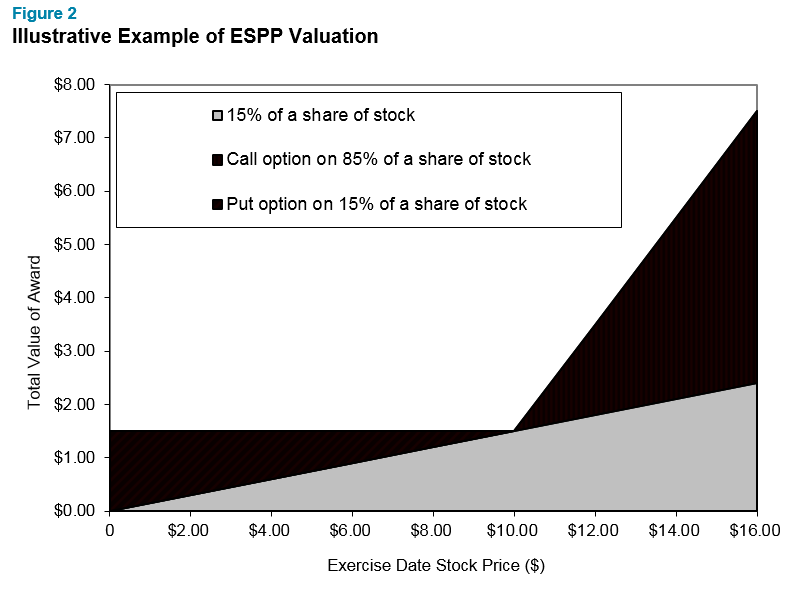

In our next example, we look at an ESPP with a six-month purchase period, 15% discount, look-back, and no interest paid on accumulated contributions. Figure 2 represents the fair value calculation.

The following chart illustrates the value of the first three of the four components of the valuation of an ESPP.

Accounting Challenges

Once the fair value is determined, the company will estimate compensation expense as of the Offering Date. The number of estimated shares to be purchased is calculated based on employee elections. Some companies factor in expected salary changes and bonuses to get a more accurate estimate and smoother expense recognition. The primary challenge in accounting for ESPPs is that the final expense is not equal to the shares purchased multiplied by the grant date fair value and some features can trigger modification accounting. That’s because there are numerous changes during a purchase period that change the number of shares ultimately purchased, and the ASC Topic 718 requires that the changes are accounted for in different ways.

The following changes occur frequently regardless of ESPP design:

- Terminations: Expense associated with terminated individuals who do not purchase shares will be reversed.

- Salary changes: When an individual’s salary increases or decreases during the period, the initial grant date share estimate is revised to reflect the actual salary during the period. This may include salary increases or estimated bonuses and commissions being more or less than expected.

- Election to decrease contributions or withdraw from the ESPP: No changes in estimated grant date expense should occur.The following two scenarios will trigger modification accounting if these features are offered in an ESPP.

- Election to increase contributions

- Rollover or Reset provision (these provisions reset the purchase price of a look-back feature)

Distinguishing salary changes and contribution changes can be especially challenging because of employees’ unique circumstances, which requires a manual expense reconciliation process. Some practical expediencies exist that generally should not result in a material difference to the overall ESPP expense. For example, contribution increases and decreases are frequently a result of employees regulating their contributions when they anticipate they will hit the IRS $25,000 limit, so the company should consider the pattern of changes or it could end up recognizing too much expense. In this example, a practical response could be to ignore individual contribution changes. We recommend discussing the overall methodology to determine ESPP expense with external auditors to ensure appropriate and compliant expense recognition.

Next Steps

The fair value calculation for an ESPP varies greatly depending on the plan design. A plan may be qualified or not, include a purchase price discount, a share match, a look-back on the purchase price, or a sales restriction after purchase. While a basic ESPP is fairly straightforward to value, some plans include more complex features that companies may not be valuing correctly or may not be incorporating into the calculation. Features such as a sales restriction or employees routinely hitting the IRS $25,000 limit or other plan limits would result in lower compensation costs if these features were factored into the calculation. Additionally, there are some design features that trigger complex accounting after the initial grant date expense is estimated. It’s important to understand the nuances of a current or contemplated ESPP and how those plan designs may impact the fair value and resulting compensation expense.

If you have questions about whether this valuation technique can be used to reduce your ESPP compensation cost, contact us at consulting@radford.com or visit us at radford.aon.com/valuation/.

Related Articles