Stakeholders are increasingly interested in how companies are improving the diversity of their boards. That interest is being reflected in the form of proxy voting, litigation and regulation. Here’s what companies should know and how they can be proactive in addressing this issue.

Public companies are under growing pressure from numerous stakeholders, including regulators, employees and institutional investors of all types, to increase board diversity. What started with a focus on gender equity has expanded into other areas, including ethnicity and, more broadly, underrepresented communities.

The governor of California signed into law Assembly Bill 979 on September 30, 2020, requiring public companies headquartered in the state to have at least one director from an “underrepresented community”[1] by the close of 2021. This new requirement comes on the heels of a previous California requirement that companies headquartered in the state have at least one female director by 2019 and two to three women (depending on overall board size) by the end of 2021. A failure to meet these obligations can result in meaningful financial penalties.

California isn’t the only state pushing for increased board diversity. The New York City Comptroller’s Office Board Accountability Project 3.0, called for 56 companies to adopt the “Rooney Rule” in searches for new board members and CEOs. The eponymous rule, named after Dan Rooney, the former owner of the National Football League’s (NFL) Pittsburgh Steelers, requires NFL teams to interview ethnic-minority candidates for senior-level jobs. Several companies have also participated in diversity campaigns, such as the 30 Percent Club, which aims as a purpose to see at least 30% representation of women on all boards and C-suites globally. And just this month, Nasdaq filed a proposal to adopt new listing rules that would require most of its listed companies to have (or explain why they do not have) at least two diverse directors, including one who identifies as a female and another who identifies as either an underrepresented minority or LGBTQ.

Outside of regulatory and legislative action, investors are also pushing for change — and not just shareholder activists. Proxy voting teams from large institutional investors, such as BlackRock and State Street, are looking for actions or policies that further the goal of increasing board diversity.

Given these developments, shareholder engagement and disclosure on board diversity are as important as ever for public companies. The stakes are high: Boards that fail to act will be called out publicy and could find themselves in the crosshairs of emerging state laws and regulations, as well as a potential target of a shareholder lawsuit.

Engagement and Disclosure on Board Diversity

In response to the growing stakeholder demand for increased board diversity, many companies have adopted and disclosed formal board diversity policies in their proxy statements. However, the level of disclosure on this topic varies, with some companies disclosing more limited, general statements that the board takes into account a diversity of backgrounds in its director selection process, while other companies have gone much further and embedded formal board diversity policy language into their nomination process. The Midwest Investors Diversity Initative (MDI) has published a document of best practices disclosure for companies looking to adopt such formal policies along with a diverse search toolkit.

There is no one-size-fits-all recommendation on this emerging disclosure, but we recommend all organizations ensure their disclosure is readily understandable and reflects concerns and input from their stakeholders.

For the past several years, investors have largely focused on gender representation on boards, as it can be difficult to assess ethnicity or other types of diverse backgrounds from public disclosure (unless a company explicitly discloses this type of information). While investors would appreciate more diversity information beyond gender, we are probably still a few years away from such increased disclosure until companies feel comfortable asking more specific information from their directors and directors are comfortable with this personal information being disclosed.

Proxy Voting and Lawsuits

Disclosure is just one element of change. Without meaningful action to boost board diversity, companies are likely to see more shareholders vote against directors’ reelection. For example, if a board does not have at least one female director (which is the case for around 40% of the Russell 3000) proxy advisory firms like Glass Lewis and Institutional Shareholder Services (ISS) will recommend investors vote against directors’ relection. (Click here to read our recent Q&A with Glass Lewis about hot topics including board diversity.)

Beyond proxy voting, boards must contend with the emerging threat of shareholder litigation. While plaintiff’s litigation around perceived excessive director compensation has been around for the last few years, we are now seeing additional litigation regarding board diversity practices. Most recently, the City of Pontiac General Employees’ Retirement System filed a derivative lawsuit on September 23, 2020, in the Northern District of California against Cisco Systems’ board of directors for a lack of African-American representation on its board. An important element of the complaint is that the plaintiff is alleging a disconnect between Cisco’s publicly disclosed policy and actual practice. “While Cisco’s publicly facing communications state that the Company is ‘committed to’ and ‘embraces’ diversity at Cisco, including at the very top, Defendants have declined to carry out the Company’s policies and proclamations have failed to increase racial diversity at Cisco,” the lawsuit states.

This is the eighth board diversity lawsuit filed in recent months, all with similar complaints to the Cisco lawsuit, and highlights a growing risk for boards in the current environment.

What is at Stake and What Should Boards Do?

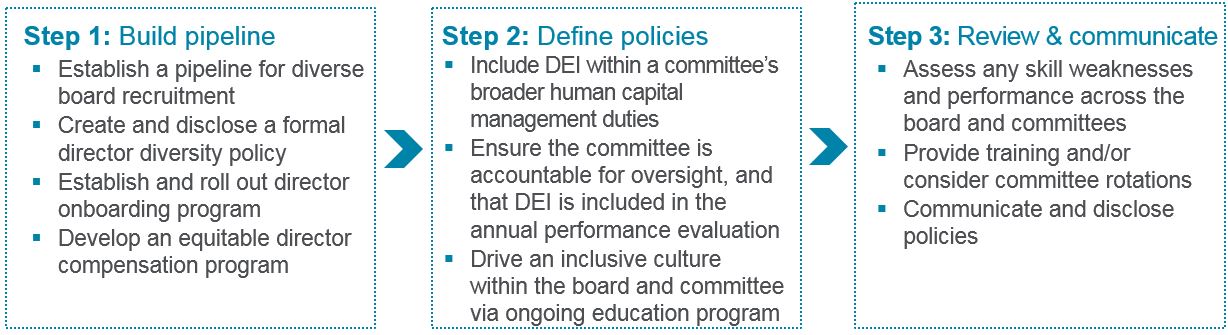

There is risk to companies’ reputation, proxy voting outcomes, board performance, and even financial impact to not creating an effective strategy for addressing board diversity. We recommend companies examine the board diversity process by taking two immediate actions. First, review current disclosure statements in the proxy statement and committee charters regarding the director nominations process. Secondly, take some level of action to develop a robust process to recruit diversified candidates. This will mitigate against these growing risks — especially at companies with no female and/or underrepresented community representation on the board. Like many topics related to environmental, social and governance (ESG) issues, companies are at different phases of their journey as it relates to board diversity. Regardless of where a company might be in that journey, it is important to consider ongoing action items, as highlighted below.

Figure 1

Three Steps to Building Greater Diversity at the Board Level

Efforts that go into developing a thoughtful board diversity plan will only translate into positive results if there is good engagement with shareholders and transparent, easily accessible disclosure surrounding these policies.

For questions about board diversity developments or other corporate governance issues, please reach out to one of the authors or write to [email protected].

[1] The legislation defines underrepresented as an individual who self-identifies as Black, African American, Hispanic, Latino, Asian, Pacific Islander, Native American, Native Hawaiian, or Alaska Native, or who self-identifies as gay, lesbian, bisexual, or transgender.

Related Articles