Changing client expectations, and an internal interest in new innovation, provide a rare opportunity for Asia’s wealth managers to revamp their service model to focus on client management activities that will benefit partnerships and empower client confidence to consolidate assets with their primary firm.

It may sound counterintuitive, but the last 12 months have affirmed that the human wealth advisor is a crucial constant in any wealth management relationship. After all, without instant and seamless access to their trusted point of contact, how else would clients gain the confidence to overcome decision paralysis in the face of long spells of volatility and economic uncertainty? If anything, their reliance on advisor expertise and insights has reinforced why the end-to-end relationship is so valuable.

What has changed, however, is high net worth (HNW) clients’ expectations of how that advice is delivered. Whereas in the past, much of the heavy lifting of client onboarding and relationship management was done by private bankers behind the scenes, now wealthy clients also want the option of a digitalised client journey that puts them in control and makes better use of their advisors’ expertise.

Some firms are already leading the way on these opportunities. HSBC continues to enhance its digital trading tools and capabilities across Asia and has launched a FinTech subsidiary to scale up wealth management offerings in China. DBS has been improving its digital wealth management app by adding smart features to anticipate clients’ investment needs.

No doubt about it, competition in this overcrowded and over-serviced space is the highest it has ever been.

Yet, changing client expectations, and an internal appetite to invest in innovations, offer a rare opportunity for Asia’s wealth managers to revamp their service model, instead of continuing to tinker with their existing digital propositions. If done correctly, valuable advisor hours could instead be spent on the client management activities that will benefit the overall relationship and empower client confidence to consolidate assets with their primary firm.

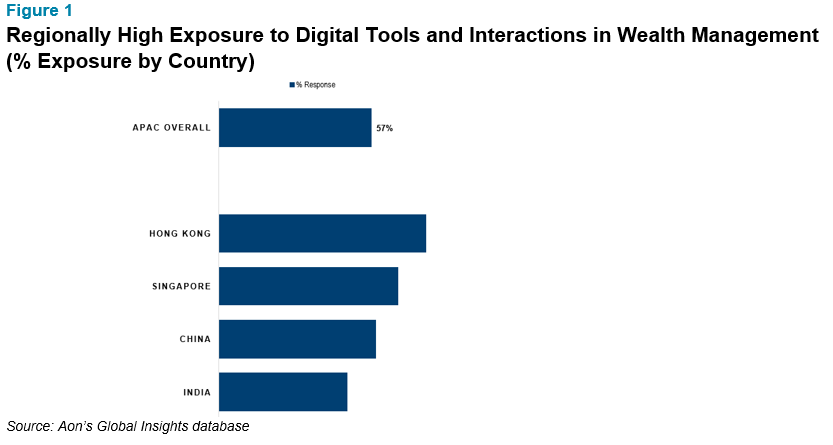

According to Aon's Global Insights database (global sample N> 2,000), 57% of Asian wealth management clients have exposure to digital tools and interactions.

Digital Adoption in Wealth: Temporary Blip or Permanent Shift?

Across APAC, high net worth individuals’ (HNWIs’) pre-pandemic exposure to self-service channels, and digital tools to manage their wealth independently, was already very high [Figure 1].

The regional figure masks some significant country differences, with clients in Hong Kong well ahead of their counterparts for exposure to digital capabilities in wealth.

The regional figure masks some significant country differences, with clients in Hong Kong well ahead of their counterparts for exposure to digital capabilities in wealth.

Digital appetites have only accelerated in the pandemic era, with fewer than 5% of Asia’s wealthy indicating that they have never used any online wealth management services.

This echoes the global trend, where online interactions between HNWIs and their wealth managers have increased during the pandemic. Many seek to maintain this frequency of online interaction, suggesting online meetings will continue to be favoured once lockdowns and travel restrictions are eased.

A Hybrid Model Needs Careful Calibration to Deliver to Client Needs

Naturally, digital engagement has led to fresh debate of how to deploy a hybrid servicing model that makes the best use of the advisor and technology, while being a win-win for clients and firms.

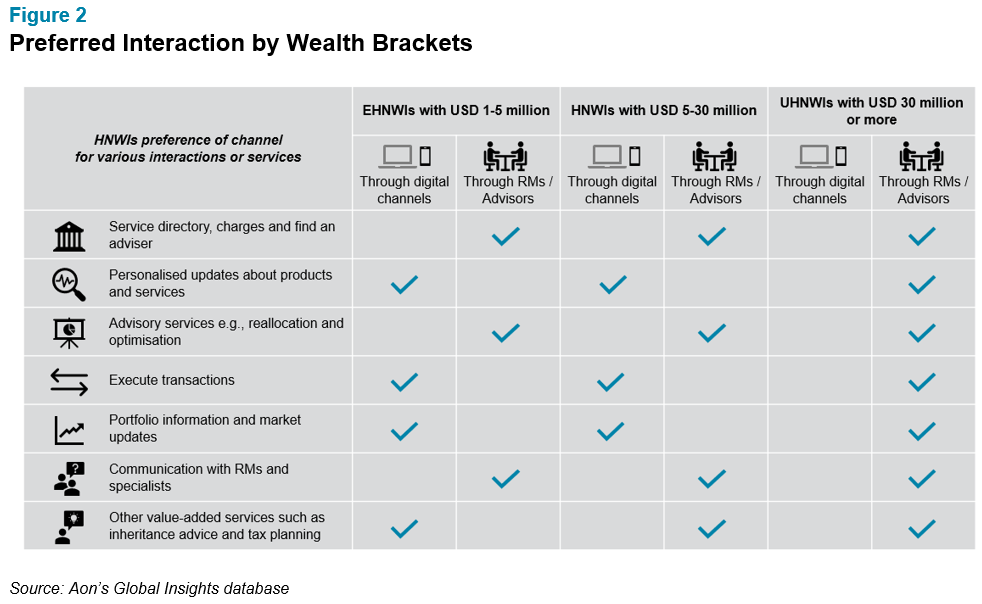

Our research findings indicate that HNWIs (with wealth of USD1-30 million) prefer to focus their digital interaction on administrative tasks, transactional processes and access to reports and information.

In contrast, ultra high net worth individuals (UHNWIs) (with wealth in excess of USD 30 million) would rather see digital capabilities deployed for personalised product and services information [Figure 2].

Hence, while the “hybrid” servicing model is preferred by a specific segment of HNW clients, it is clear that clients want digital tools to be deployed predominantly on tasks that do not influence investment outcomes.

This could still be extremely beneficial to the overall client experience if straightforward tasks can be completed with greater speed, transparency and accessibility. At the same time, transactional activities would be taken off advisors’ plates, boosting productivity and allowing them to focus on more complex challenges.

There is Already an Exception Gap in the Client Experience

The situation today reveals that there is still a long way to go to fully meet and deliver clients’ expectations. Many wealth managers do not perceive their primary wealth management providers as ‘digital leaders.’

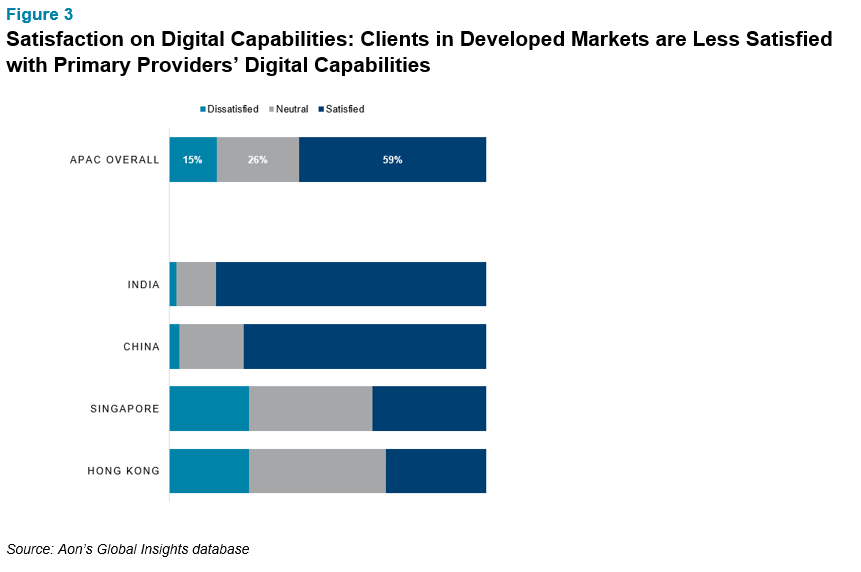

Among HNW clients (with USD 1-30 million), close to half are not satisfied with the digital capabilities offered by their primary provider [Figure 3]. In Hong Kong and Singapore, the wealth hubs of APAC, only 1 in 3 HNWIs is satisfied.

In contrast, clients in emerging markets like China and India are relatively more satisfied with the current digital capabilities of their primary provider.

According to Aon's Global Insights database (N> 2,000), 59% of clients in Asia are satisfied with their providers' digital capabilities.

Catering to Different Client Profiles

There are many improvement areas for traditional wealth management providers to meet clients’ rapidly evolving demands. Firms will need to consider how best to generate trust and confidence as they transact throughout their digital journey.

This is particularly salient in Hong Kong, where close to 80% of clients do not feel they are offered a choice on how they can transact with their primary wealth management provider (i.e. self-service or by an advisor). Less than 30% claim the digital channels provided are sufficiently user-friendly (Source: Aon’s Global Insights database).

Many Hong Kong clients are self-directed investors and comfortable proactively sourcing insights to make trades and investment decisions independently. As a result, they need a digital platform with comprehensive functionality, from daily transactions to real-time updates and trading capabilities.

Conclusion

There is an irreversible trend in APAC towards digitalisation irrespective of wealth, generation or country. As clients’ expectations and demands of digital services are already high, it seems unlikely that the current services available – which only do a mediocre job of meeting clients’ needs – will be sufficient to guarantee their loyalty in the long-term.

Firms should keep themselves up to date on what clients perceive as important in their digital ecosystem, using client insight on their wealth journey to segment which activities can be automated to the benefit of both sides.

Although competition is stiff, there are plenty of opportunities for traditional wealth management firms to learn from leaders in this area, build upon their existing expertise and reputation, and innovate in the digital space.