Introduction

We've all heard the age-old adage "time is money." For companies seeking to hire their first chief financial officer (CFO) in preparation for an initial public offering (IPO), the relationship between time and money can take on numerous meanings. Depending on how close a CFO is hired to an IPO, it can change the date of an offering, it can alter the very nature of how a company is valued, and it can influence how a new CFO is paid. Of course, for our team at Radford, the latter issue is most near and dear to our hearts, so we set out to discover whether or not the timing of when a CFO is hired in preparation for an IPO has predictable implications on his or her pay.

Why study CFOs? Unlike chief executive officers and product development executives, who often nourish a startup from infancy to an IPO, CFOs are generally on-boarded much closer to an offering. At technology and life sciences companies that have gone public since the start of 2013, the median tenure of a CFO was just 2.3 years at the time of IPO. In contrast, the median tenure for CEOs was 6.2 years. Additionally, in the current frenzy of public listings, the competition for proven CFO talent is fierce. While some companies grow a senior member of the finance team into the CFO role, most look to hire from the outside in a quest for prior experience and a proven track record. All of these factors make the market for pre-IPO CFO talent highly active and dynamic.

To meet market demands, companies typically attract CFO candidates with large equity grants. These grants, which can include new-hire and ongoing awards, often add up to nearly 1% of the company by the time an IPO is reached. According to Radford's analysis of data from 39 technology companies and 38 life sciences companies that went public between Jan. 1, 2013 and June 30, 2014 (and had quality disclosure of CFO on-boarding packages), we found that the median technology CFO can expect to own 0.96% of the company at the time of an IPO through new-hire equity awards and additional top-up grants in the months preceding an offering. At life sciences firms, the median equity ownership level is 0.81%.

Once public, this ownership translates into tangible value. Technology CFOs held a median of $4 million in equity (both vested and unvested) at IPO—equivalent to nearly 15 times the median CFO's annual base salary of $270,000. In the life sciences sector, the median CFO can expect to hold $1.3 million in equity, approximately 4.5 times his or her base salary.

Given the magnitude of this data, Boards and venture capital investors at pre-IPO companies are increasingly interested in understanding how tenure prior to an IPO should impact award size. They are also searching for the optimal time to hire a new CFO, both from the perspective of managing costs and making the right financial offer at the right time.

Total Potential Equity Ownership

In an effort to begin understanding the varying costs of hiring a CFO prior to an IPO, Radford first researched total potential equity ownership. This value expresses the total number of shares held by an executive as a percentage of post-IPO total common stock issued and outstanding. Shares held by an executive can include shares owned outright, vested unexercised stock options, and unvested equity awards (either options or restricted stock).

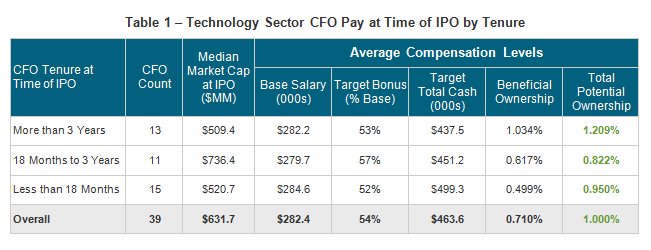

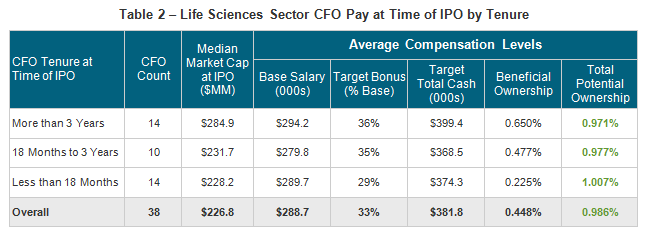

Using the same sample set of companies described in the opening of this article, the following tables display the relationship between a CFO's tenure at the time of an IPO and their total potential ownership.

If you approach the results of our analysis from the perspective that companies probably don't spend enough time considering how tenure at IPO should impact equity ownership levels, then the information presented above is probably not surprising. No matter how you slice the data by CFO tenure at IPO, total potential equity ownership is close to static at roughly 1%. In other words, regardless of when a CFO joins a private company, they can expect to receive a similar amount of overall equity by the time an IPO arrives. The stagnant nature of these results also means that the timing of when a CFO is hired in preparation for an IPO currently has little impact on expected dilution for shareholders— from a cost to shareholders perspective, the answer is always about 1%.

Interestingly, cash compensation practices, whether you look at base salaries, target bonus opportunities or target total cash opportunities also vary little by tenure at IPO. Since our data examines pay levels at the time of an IPO, we believe two forces are likely driving this result: (1) companies broadly view all private companies, regardless of stage, as one large benchmarking market; and (2) companies usually begin to migrate cash compensation to public companies practices very close to going public, leading to fairly consistent pay levels by the time an IPO arrives.

We also tracked beneficial ownership in our study, which is equity that is owned outright or vested. As one might expect, beneficial ownership increases with tenure. This measure highlights how much ownership could be liquid, or near liquid (once holding periods end), at the time of an IPO.

Total Potential Equity Value

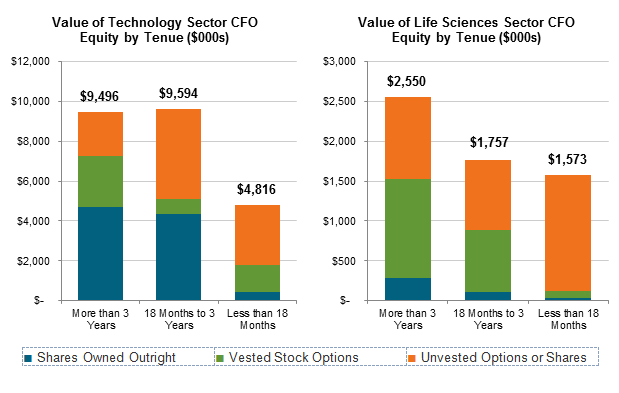

While there appears to be no significant relationship between CFO tenure at IPO and overall equity ownership levels, it stands to reason that the potential value of equity awards could vary significantly by tenure. At a minimum, employees who join a company years before an IPO should benefit greatly from lower initial strike prices on their stock options. This effect should be magnified at private technology and life sciences companies, which rely very heavily on equity awards and specifically stock options.

When we examine the value of equity holdings by tenure (again using the same sample group described in the opening of this article), our assumptions generally prove to be true across the technology and life sciences sectors. CFOs with more tenure at an IPO typically hold more overall equity value. And as expected, the value of vested and/or unvested options plays a big role.

For the purposes of our analysis, the values of CFO equity holdings were calculated by looking at three categories of shares as follows: shares owned outright, vested options, and unvested options or shares. Shares owned outright and unvested shares (e.g., restricted stock) were valued at the IPO price. Vested options and unvested options were valued using the spread between strike prices and the IPO price.

Conclusion

When Radford set out to conduct research on CFO hiring costs at pre-IPO companies, our primary point of interest was to examine potential connections between pay practices and tenure. On several fronts, the results of our study point to no meaningful differences in pay practices based on tenure at the time of an IPO. These areas include base salaries, bonus targets and overall equity ownership as a percentage of the company. The lack of diversity in overall equity ownership levels is particularly interesting, as the amount of equity delivered to a CFO directly impacts shareholder dilution.

On one hand, consistency of practice at all points in time leading up to an IPO could be reassuring to investors— this makes it incredibly easy to predict the dilutive cost of a CFO. On the other hand, our data begs the question of whether or not there should be more differentiation in the market to optimize outcomes for shareholders and to deliver the right balance of risk and reward to employees based on when they join a private company.

Perhaps these questions have not become a hot topic of debate in past years because of the one significant area where tenure impacts pay outcomes, namely the value of equity holdings at the time of an IPO. Here our data meets expectations and points to meaningful differentiation by tenure. These results are primarily driven by the value of vested and unvested stock options, which are generally far more advantageous to employees who join a company well before an IPO.

In terms of next steps, we believe this data suggests that private companies may want to consider hiring a CFO sooner than originally planned. If pay practices and cost implications are generally consistent regardless of when a CFO is hired, then there is little benefit in waiting. A CFO hired earlier will end up owning roughly the same percentage of the company as a CFO hired late in the game, but will have more value on the table leading to retention benefits for the company up through an IPO. Plus, there are other non-compensation benefits related to hiring a CFO earlier in the process of going public: longer-tenured CFOs will have more time to develop an understanding of the company's business model, establish relationships with the executive team and prepare for the offering event itself.

Given these advantages, we can conclude that venture capitalists looking to maximize their return on investment, not only on the balance sheet but in their human capital, could be well-served to think early about hiring an experienced CFO that can help the company through its next growth chapter.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles