Relative to the rest of Europe, Nordic biotech companies are far more conservative in their use of equity awards for executives, issuing fewer shares and performance-based awards.

The market for biotech talent is increasingly global. Employee mobility and connectivity are on the rise at all levels, but these trends are particularly impactful in the executive suite. Boards now routinely search for executive candidates across Europe, and companies (even very small firms) increasingly have executives in multiple locations. However, recruiting on a global scale can create unforeseen challenges, especially when structural rewards practices differ dramatically across countries. We see these challenges first hand in our work with clients in the booming Nordic biotech market. There, equity programs are far less aggressive than the rest of Europe and, to an even larger degree, the United States (US), sometimes making it very difficult to attract top talent.

To put things into proper perspective, European biotech firms continue to be more modest and risk adverse in their use of equity compensation relative to the US. Equity award values in Europe tend to be lower, and equity plans are generally more shareholder-friendly in their design. Yet, even by European standards, the Nordic region stands out as especially conservative when it comes to annual equity usage (i.e., burn rates) and overall employee ownership levels (i.e., equity overhang).

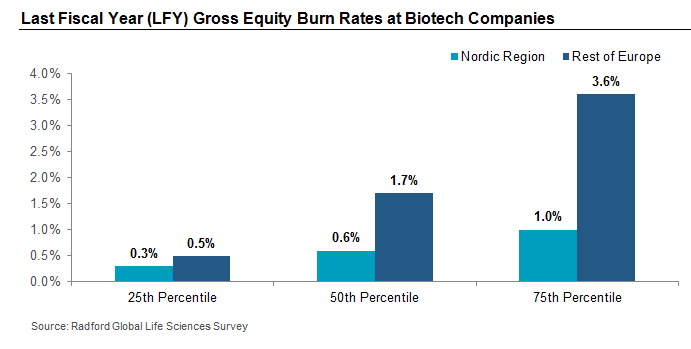

Looking first at annual equity delivery, the median Nordic biotech company has a last fiscal year (LFY) gross equity burn rate of 0.6%. In other words, employees received 0.6% of the company last year. This compares to median LFY gross burn rates of 1.7% for biotech firms in the rest of Europe. This gap is significant, and represents a nearly 3x multiple in equity usage at European biotech companies outside of the Nordic region.

This gap narrows significantly at the 25th percentile of the market; however, at the 75th percentile of the market, the differences between Nordic-based firms and the rest of Europe accelerate slightly— the annual equity usage multiple increases to 3.6x. The following chart illustrates this dynamic using our most recent data from the Radford Global Life Sciences Survey.

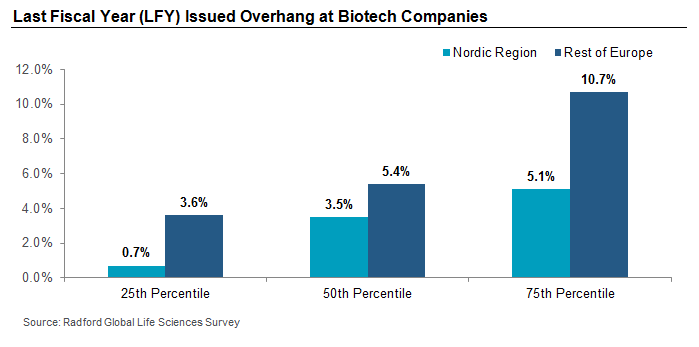

Given the fact that annual equity usage tends to be much lower in the Nordic region, it follows that aggregate employee ownership, or equity overhang, is also lower in the region. At the median of the market, LFY issued equity overhang is 3.5% for biotech companies in the Nordic region. This compares to a median LFY issued overhang of 5.4% for the rest of Europe. And once again, as the chart below illustrates, differences are even more pronounced at the 75th percentile of the market.

While investors will appreciate lower rates of dilution, delivering such reduced levels of equity compensation relative to the rest of Europe can put Nordic-based biotech companies at a disadvantage when attracting talent on a regional or global basis. What's more, the disparities between Nordic-based biotech firms and the rest of the Europe do not end there. Equity plan design practices also differ in many important ways, and may create additional recruiting challenges for Nordic companies.

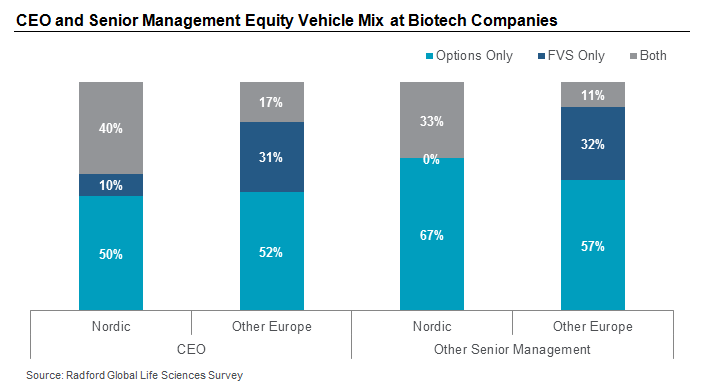

To explore this point further, we next examined equity vehicle mix at biotech companies across Europe. While the most prevalent form of equity delivery among all European biotech firms, including in the Nordic region, is the exclusive use of stock options, practices vary more widely at the edges. Today, a significant minority of European biotech firms outside of the Nordic region (31%) use full value shares (FVS) exclusively for their CEOs. However, just 10% of Nordic firms use this approach for their CEOs. This is significant because full value shares are often tied to performance-based vesting conditions, which is an increasingly common practice across the overall life sciences sector in both Europe and the US. As the chart below shows, similar variations in practice also exist for senior management roles.

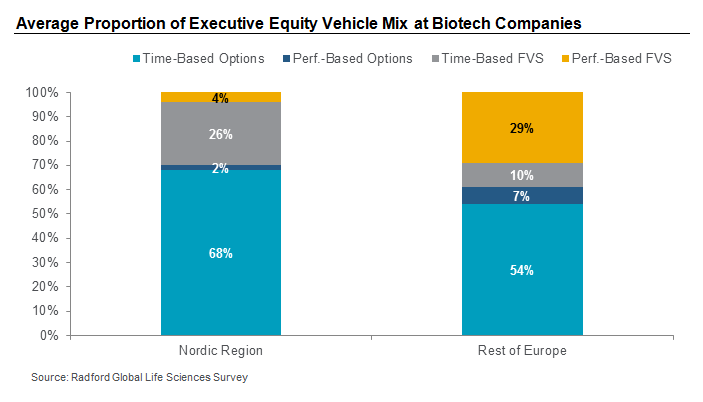

Still, the prevalence of equity vehicles in use only tells us one side of the story. A more complete picture can be gained by examining the average mix of equity value delivered by vehicle to executives. When looking at this data, we arrive at the same basic conclusion as above. In both the Nordic region and the rest of Europe, executives at biotech companies receive most of their annual equity value in the form of time-based stock options, nearly 70% and 55% respectively. However, equity value mix varies significantly for the remainder of what executives receive. In the Nordic region, nearly all additional equity value arrives in the form of time-based full value shares. Conversely, as we alluded to before, for biotech executives in the rest of Europe, almost all of the additional equity value arrives in the form of performance-based full value shares.

Next Step

As we've shown, equity practices at Nordic-based biotech companies are fundamentally different than the rest of Europe. Nordic-based firms grant far less equity to employees and senior leaders, and remain more reliant on stock options and time-based vesting schedules. Meanwhile, the rest of Europe typically delivers much more equity to employees, and that equity is increasingly tied to performance-based vesting conditions.

Giving employees, especially executives, less equity ownership (i.e., less long-term upside) likely hinders recruitment efforts. Nordic executives are clearly at a comparative disadvantage relative to their European peers. And while it could be argued that granting a larger proportion of equity awards with time-based vesting creates less compensation risk for Nordic executives, this slight advantage could be a short-lived one.

Equity plan design practices at European biotech companies continue to evolve, and while we observe significant differences between the Nordic region and the rest of Europe today, the landscape is changing and likely to converge in the coming years. As more executive and board talent moves across country boarders, this will naturally lead to a merger of rewards practices and philosophies. And perhaps most importantly, as more European companies are pressured by institutional investors and governance bodies to migrate toward delivering a greater share of equity tied to performance metrics, it's hard to see a scenario where Nordic firms will be able to escape these forces. The pending revision to the Shareholder Rights Directive in Europe, if enacted, will also play a central role in accelerating this change. Finally, we also see the impact of US practices in the Nordic region, particularly among Nordic-headquartered companies that are listed on the Nasdaq exchange. Against this noisy backdrop, Nordic biotech companies need to at least be more aware of how their equity practices differ from the rest of the world in this increasingly global sector.

To learn more about participating in a Radford survey, please contact our team. To speak with a member of our compensation consulting group, please write to consulting@radford.com.

Related Articles